Summary and Price Action Rundown

Global risk assets are extending their ongoing rally morning as investors take an upbeat posture into tomorrow’s start of second quarter corporate earnings reporting season despite continually rising US Covid-19 cases and simmering US-China tensions. S&P 500 futures indicate a 0.7% higher open after the index advanced 1.8% last week to pare its year-to-date downside to 1.4%, while the tech-heavy Nasdaq is poised to register another new record high. Equities in the EU are posting solid gains ahead of a key regional summit this week and a European Central Bank meeting on Thursday, while Asian stocks are continuing to outperform. The dollar is steady and longer-dated Treasury yields are hovering above recent lows, with the 10-year yield at 0.65%. Brent crude prices are retreating below $43 on OPEC+ headlines.

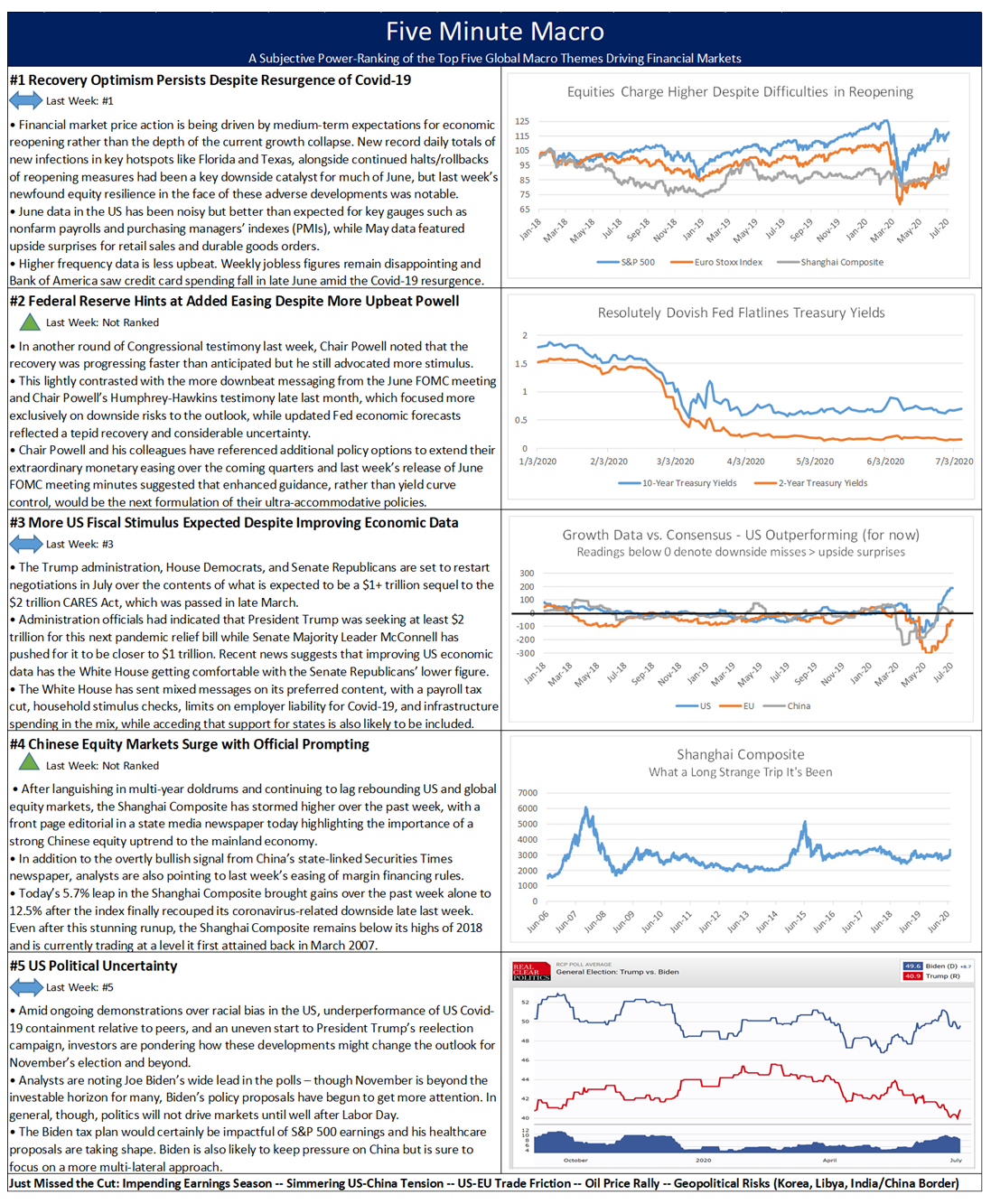

China’s Recovery Remains in Focus as Mainland Equities Soar

Upbeat commentary from China’s central bank, improving economic data, and continued upside for Chinese stocks support global sentiment despite incremental escalation of US-China tensions. An official at the People’s Bank of China told reporters last week that stimulus measures had run their course given that the economy will “return to normal” in the second half of this year. This comes ahead of China’s release of second quarter (Q2) GDP on Thursday, along with monthly readings for fixed asset investment, industrial output, and retail sales for last month, all of which are expected to show improvement. Regarding GDP, the consensus is for a rebound following the prior quarter’s historic 6.8% collapse, with estimates of a 2.5% expansion in the three months through June. There have been numerous signals of accelerating recovery in China after the depths of the pandemic. Overnight, South Korea’s report on exports for the first ten days of July was upbeat, showing a year-on-year (y/y) contraction of 1.7% after a -11% y/y reading for June, with exports to China outperforming with a 9.4% y/y increase to start this month. Nevertheless, Premier Li conveyed caution over the rebound, saying that conditions remain “severe.” Meanwhile, US lawmakers, including Republican Senators Rubio and Cruz, House Representative Chris Smith and Ambassador Brownback, are being sanctioned by China in retaliation for the Trump administration last week sanctioning senior Chinese party leaders over their involvement in repression of Uighur Muslims in the Xinjiang province. These escalatory moves have largely been interpreted as symbolic and scant details were provided. Price action indicates that investors are focused on China’s upside potential rather than friction with the US. Foreign capital flowed into locally denominated Chinese government bonds in Q2 at the fastest pace since late 2018, according to data from CEIC, an economic data provider, topping 4.3 trillion renminbi ($619 billion), the highest on record. Also, local equities remain exceptionally buoyant, with the Shanghai Composite rising another 1.8% overnight to put month-to-date gains for benchmark index at 15.4%. Lastly, the renminbi is stable at its strongest level versus the dollar since mid-March, having appreciated 2.3% since late May.

OPEC+ Set to Taper Supply Curbs

Oil is not participating in today’s broad risk asset price gains following headlines indicating that coordinated output cuts that have been instrumental in supporting crude prices will start to be dialed back next month. OPEC’s technical committee will meet this Wednesday to review ongoing compliance with agreed curbs but will also reportedly discuss the approach to easing those commitments over the coming months. Russia is said to be preparing to lift its production in August absent any agreement to extend the current level of cuts. For context, 9.6 million barrels per day (bpd) of potential are being held back by the cartel and its allies, and reports suggest that delegates are pressing for a reduction of that amount to 7.7 million bpd for August and progressively lower thereafter. Oil prices are moderately lower on the news, with renewed threats to supply from Libya helping provide some upside support. After rallying sharply in May, international benchmark Brent crude has struggled to make headway above the low $40 per barrel range, while US benchmark WTI has been similarly stalled in the high $30’s per barrel.

Additional Themes

Vaccine News Overbalances Grim Covid-19 Outbreak News – After US equities recouped early losses and closed higher on Friday after drugmaker Gilead announced positive results for its coronavirus therapeutic Remdesivir, market spirits are being lifted again today by news that possible vaccines developed by Pfizer and BioNTech have been granted “fast track” status by the FDA. Shares of Pfizer and BioNTech are up 2.0% and 5.5% in pre-market trading. Analysts note that accelerating cases in US hotspots like Florida are no longer weighing on sentiment to the extent they did in June as mortality rates are rising are a proportionately slower pace.

US Banks in the Spotlight – After an index of bank stocks gained 5.3% on Friday, analysts are pondering whether the momentum can continue ahead of earnings reports for the sector, which kick off tomorrow with Citigroup, JPMorgan, Wells Fargo, and First Republic reporting.