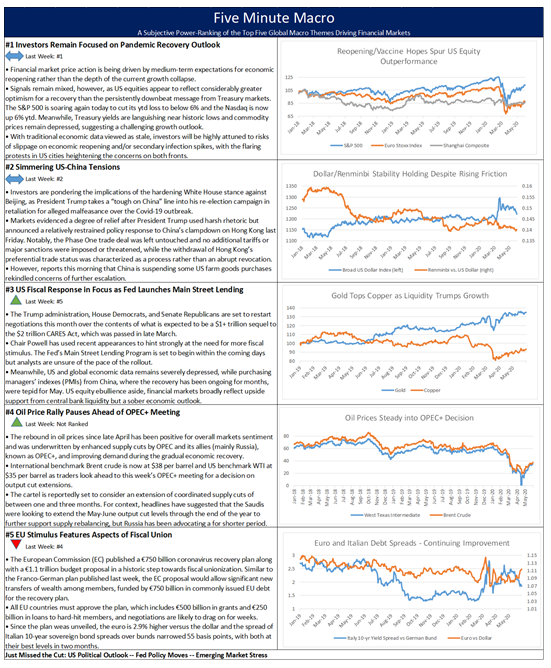

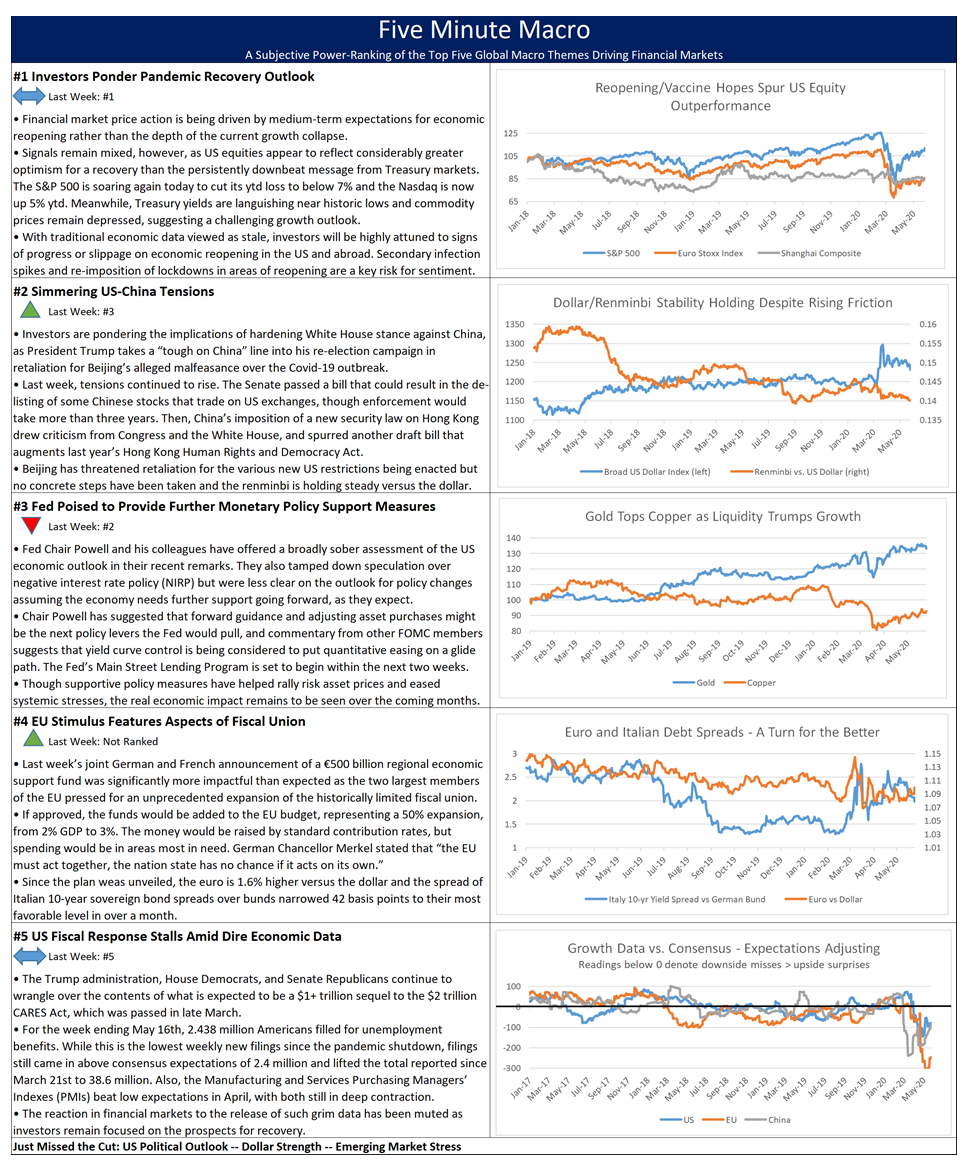

Summary and Price Action Rundown

Global risk assets were mostly higher overnight as investors noted continuing unrest in US cities but focused on economic reopening and recovery prospects, though oil prices paused their rally amid OPEC intrigue. S&P 500 futures point to a 0.4% higher open, which would extend yesterday’s 0.6% gain that put the index’s year-to-date downside at 4.6% and the decline from February’s record high at 9.0%. Equities in the EU are continuing to outperform while Asian stocks extended their gains as well. Longer-dated Treasury yields are edging higher within their narrow range, with the 10-year yield at 0.70%. Meanwhile, the dollar is deepening its ongoing decline as the euro continues to rally, though the renminbi slipped lower overnight. Crude oil had reached a new multi-month high earlier this morning but is retreating amid doubts over the OPEC meeting that was provisionally scheduled for this week (more below).

EU Assets Continue to Rally

Better-than-anticipated data and moves toward reopening more of the regional economy are extending the outperformance of EU stocks and the rebound in the euro against the dollar. The final reading of the May service sector purchasing managers’ index (PMI) for the EU printed 30.5 versus an initial reading of 28.7, which still reflects sharp contraction of activity but at an easing pace and is the best level since February. May’s composite PMI, which combines services and manufacturing gauges, registered 31.9 versus a preliminary reading of 30.5, which is also the highest level since February and well below the deep abyss of April. Importantly, the PMI readings for Italy, which has been the EU country hardest hit by the pandemic, showed some of the steepest improvement from the initial reading for May and April’s historic lows. For context, PMI readings below 50 denote a slowing of activity in the sector. Meanwhile, unemployment for EU only edged higher to 7.3% in April from the prior month’s 7.1%, bettering consensus expectations of 8.2%. Adding to the positive tone in regional markets are reports that Germany’s government is preparing to downgrade its travel warnings and restrictions this week. These developments are helping extend the outperformance of EU assets that has been largely underwritten by hopes for additional stimulus, with German Chancellor Merkel pushing for additional fiscal support for the EU’s largest economy and member nations negotiating a historic €750 billion pan-EU pandemic relief budget that represents a vital step towards fiscal unionization. Since May 18th, when France and Germany unveiled their plans for this relief budget, the Euro Stoxx index is up 16.3%, handily outpacing the 7.6% gain for the S&P 500 over that period, while the euro is 3.6% stronger versus the dollar and the yields on peripheral EU debt, like Italian and Spanish bonds, continue to converge toward German bund yields. – MPP view: To be fair, the recent outperformance of EU assets does represent a degree of catch-up after lagging on this rebound, but if the EU looks set to emerge from the pandemic with stronger internal bonds than before, that stands in sharp contrast to most everywhere else.

Questions Mount Ahead of OPEC+ Meeting

Oil prices are wavering this morning following reports that Saudi Arabia is threatening to suspend the meeting of OPEC and its allies (collectively known as OPEC+) this week barring firm commitments from countries like Iraq and Nigeria to honor output cut commitments. As traders awaited official confirmation of the virtual meeting of OPEC+, which had been provisionally schedule for tomorrow, headlines this morning put the cartel summit in doubt. Saudi’s reported hardline approach to overproduction among some members is threatening consensus expectations for a one-month extension through July of the 9.7 million barrels per day output cuts, which is being pushed by Russia and its allies. Saudi’s position on this proposal has remained unclear, though the Kingdom had reportedly been looking to push the May-June output cut levels through the end of the year to further support supply rebalancing. Another unknown is whether Saudi, Kuwait, and the UAE would extend their volitional additional cuts of 1.2 million barrels per day alongside any broader extension. Crude prices have retreated this morning from their highest levels since early March, even as a report from the American Petroleum Institute pointed to a further drawdown of US crude stockpiles this week. – MPP view: Commitments to cartel supply cuts were always going to get wobbly as prices rise and now reports indicate that shale patch shut-ins are slowing. If tomorrow’s Baker Hughes US active drill rig count indicates that shale production may be bottoming, it will mean that OPEC+ will have a steeper uphill climb over the coming months even if it does manage to agree on a short output cut extension. The oil price rally has been impressive and has gone farther than we anticipated, but this OPEC+ episode will be a key test.

Additional Themes

US Unrest Draws Scant Market Reaction – Reports indicated a relatively more peaceful overnight in US cities after a string of nights marked by violence. – MPP view: Wall Street is not alone in its confusion over the potential significance of the whipping political winds in the US, but generally speaking it is hard to trade the election until after Labor Day.

Zooming Earnings – Yesterday after the market closed, Zoom Video Communications reported its triumphant Q1 earnings report, topping estimates by $0.10 with an earnings-per-share (EPS) value of $0.20. Revenue of $328.2 million beat projections by $124.6 million and exceeded last year’s amount by 169%. As Covid-19 quarantine measures were strictly instated, many business operations and social interactions have moved to online platforms resulting in soaring growth for companies like Zoom. Counter to the trend of the recent earnings season, Zoom has proudly declared its 2021 forward guidance expecting Q1 2021 to be between $495 million and $500 million. The stock price is 0.4% higher pre-market, furthering its climb of 205% for the year.