Summary and Price Action Rundown

Global risk assets are were mostly higher overnight as upbeat news on development of a Covid-19 vaccine inoculates investor sentiment against mixed US corporate earnings and discouraging developments on pandemic containment. S&P 500 futures indicate a 1.2% gain at the open after yesterday’s 1.3% rally brought the index within 1% of turning positive for the year. Equities in the EU are rising, while Asian stocks mostly gained despite underperformance of the Shanghai Composite. The dollar is retreating amid a diminishing safe-haven bid, while longer-dated Treasury yields are only edging above recent lows, with the 10-year yield at 0.64%. Brent crude prices are back above $43 as OPEC and its allies meet today.

Loan Loss Preparations Weigh on Bank Earnings

Second quarter (Q2) earnings season continues today after yesterday’s uneven start, as three US megabanks issued varied results amid preparations for further deterioration in credit conditions due to a halting economic recovery. Reports from Goldman Sachs, PNC Bank, Bank of New York Mellon, and US Bancorp will make headlines before today’s opening bell. JPMorgan, Citi, and Wells Fargo kicked off reporting for the sector with mixed results yesterday, resulting in disparate stock price performance of 0.6%, -3.9%, and -4.6%, respectively, on the day. Citi and JPMorgan both beat earnings-per-share (EPS) estimates and revenue projections, though Wells Fargo undershot both their top and bottom-line forecasts. Wells Fargo CEO Charles Scharf partially blamed the asset cap placed on banks by the Federal Reserve as it restricted the bank’s ability to grow its balance sheet to offset the lower interest rate environment. Wells Fargo cut its quarterly dividend down to $0.10 from $0.51. Analysts were particularly focused on the degree of credit provisioning, and all three banks bolstered loss reserves more than had been expected. JPMorgan funded a massive injection into credit-loss reserves totaling just shy of $9 billion, while Wells Fargo and Citi boosted theirs by $8.4 billion and $5.6 billion, respectively, with all three citing heightened economic uncertainty. While building these credit cushions signals caution, it has put the banks on increasingly solid systemic footing ahead of any upcoming Covid-related stressors, with credit default swaps on each of yesterday’s reporting institutions remaining at tame levels. Offsetting the drag, Citi and JPMorgan received a boost from strong trading and investment banking during the quarter, areas in which Goldman Sachs is expected to show solid performance in their release this morning.

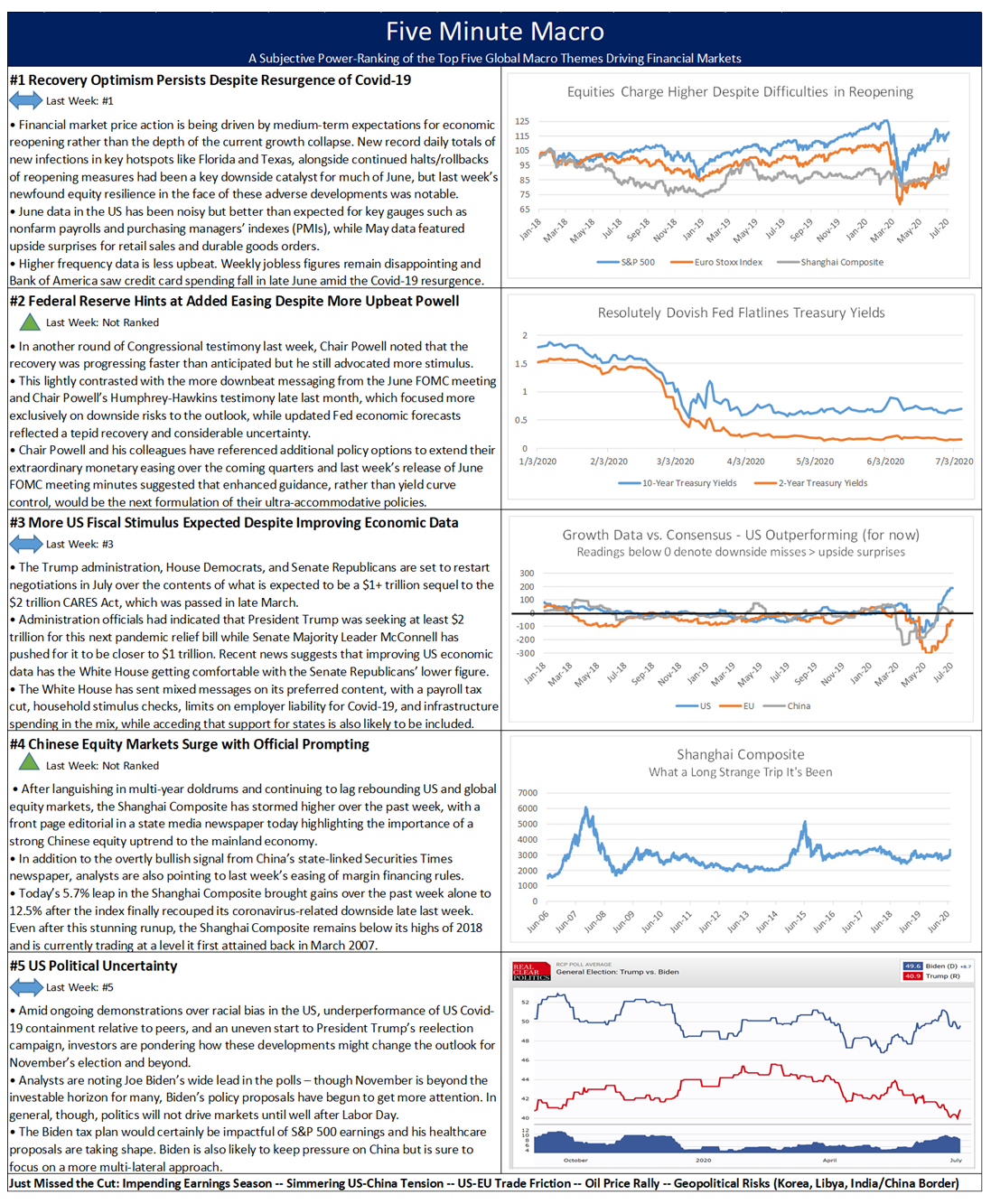

Global Central Banks Remain Cautious

Federal Reserve communications continue to center on downside risks while the Bank of Japan retained its ultra-accommodative posture overnight, with the Bank of Canada expected to augment its asset purchases today. Yesterday, analysts noted downbeat commentary from FOMC member Lael Brainard who cited a “thick fog of uncertainty” in which “downside risks predominate.” Against this grim backdrop, Brainard advocated a pivot in Fed policy “from stabilization to accommodation,” citing goals of full employment and inflation at its 2% target. Analysts speculate that these aspects of the dual mandate will be used as benchmarks for a new form of enhanced forward guidance that could be revealed as early as the September meeting. Meanwhile, overseas, the Bank of Japan kept its key short-term interest rate at -0.1% and maintained the target for the 10-year Japanese government bond yield at around 0% at its July meeting, by an 8-1 vote to match market expectations. It also pledged to continue supporting firms through its $1 trillion equivalent special financing program. In its quarterly outlook report, the central bank said that Japan’s economy is likely to improve gradually from the second half of this year, though only moderately as Covid-19 impedes growth worldwide. The 2020 fiscal year GDP forecast was refined to -4.7% and CPI to -0.5% from April’s less-defined range of projections. The yen is posting modest appreciation versus the dollar this morning but remains within its recent trading range. Later today, the Bank of Canada is expected to bolster its asset purchase program to buy more government bonds. The Canadian dollar, like the yen, has not evidenced a strong trend versus the US dollar over the past month.

Additional Themes

Oil Prices Rise as OPEC Meets – Oil prices are rising this morning amid reports that today’s cartel meeting will yield a smaller-than-expected taper of ongoing crude output curbs. Member countries that had lagged in implementing the cuts are now expected to provide some compensatory restraint over the coming months.

Return to Lockdown Depresses Australian Consumers – Consumer confidence in Australia tanked on the news of re-imposed restrictions for the spike in Covid-19 infections. The Melbourne Institute and Westpac Bank Consumer Sentiment Index for Australia declined by 6.1% month-on-month (m/m) to 87.9 in July 2020, ending a two-month rally after a 6.3% rise in June thanks to a renewed surge in Covid-19 cases in Victoria and following reintroduction of lockdown restrictions in Melbourne. Economic conditions for the next 12 months recorded the biggest fall, tumbling 14% to 66.4 amid fears that the damage from the virus would be prolonged. Conditions for the next 5 years plunged 10.3% to 91.9, and finances for the next 12 months sub-index sank 6.7% to 98.3. The Australian dollar, however, is up 0.7% versus its US counterpart today amid the general optimism surrounding a Covid-19 vaccine.