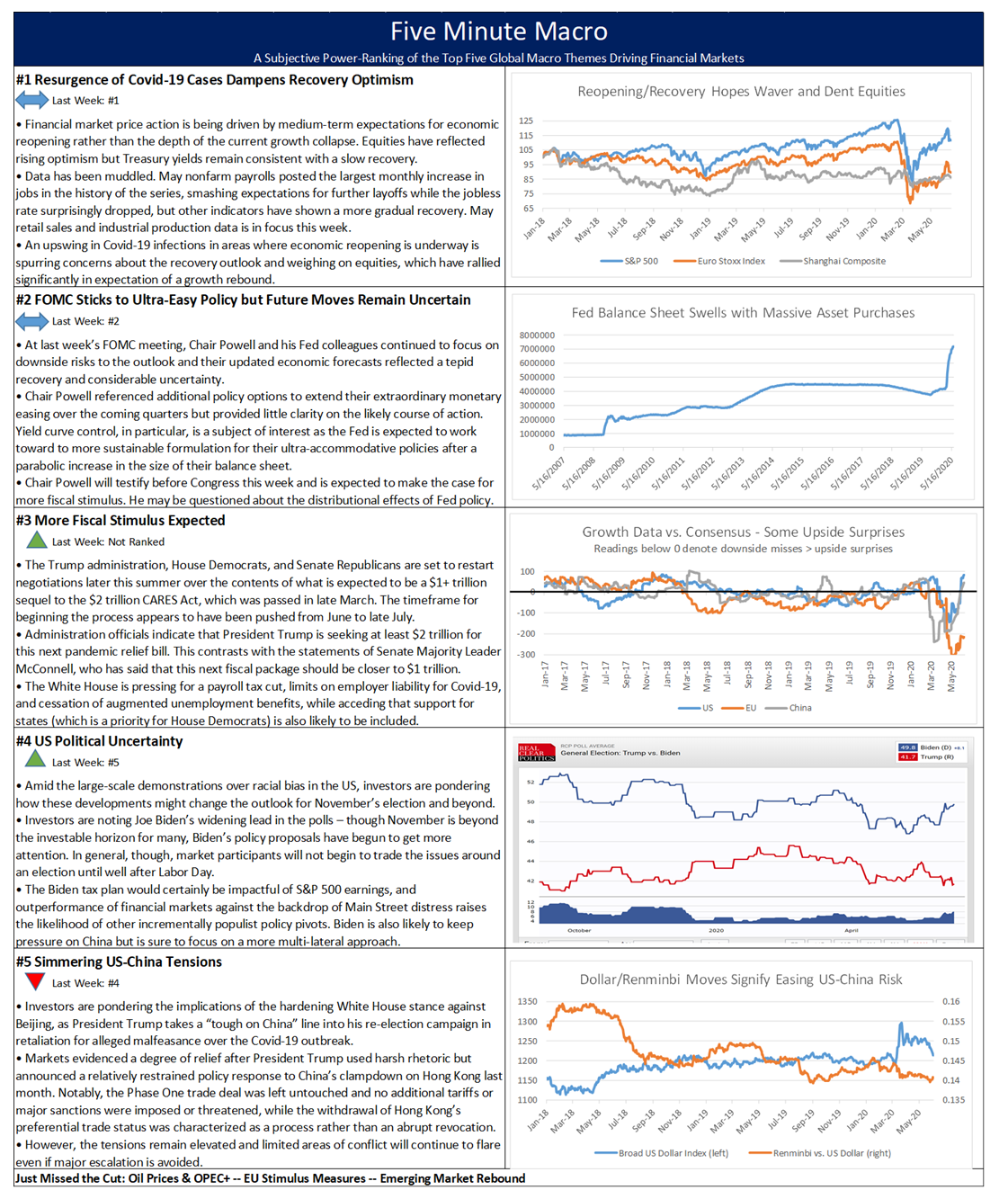

Covid-19 resurgence dampens recovery optimism remains front and center followed by Fed Policy and the size and timing of CARES Act 2. Finally, US Political Uncertainty and Simmering US-China Tensions round out the top five.

Covid-19 resurgence dampens recovery optimism remains front and center followed by Fed Policy and the size and timing of CARES Act 2. Finally, US Political Uncertainty and Simmering US-China Tensions round out the top five.

Summary and Price Action Rundown

Global risk assets moved sharply lower overnight as investors continue to grapple with the risk that a secondary spike in Covid-19 infections will impede economic reopening. S&P 500 futures indicate a 2.2% lower open after the index suffered its first weekly decline in a month last week, sliding 4.8%. The sharp rally for the S&P 500 in prior weeks had erased the index’s year-to-date downside as of last Monday. Equities in the EU are similarly lower while Asian stocks posted some steep declines overnight. Longer-dated Treasury yields have reverted to their previous range, with the 10-year yield descending to 0.67% this morning, while the dollar is edging higher. Crude oil is lower, with Brent dropping toward $38 per barrel.

Covid-19 Resurgence Risk Weighs on Investor Sentiment

Last week’s abrupt return of market volatility, which many analysts ascribed in part to the rising number of coronavirus cases in areas that have been in the process of economic reopening, is set to continue today as infection data continued to worsen over the weekend. Texas, Florida, Georgia, Arizona, North Carolina, and South Carolina are among the states experiencing a rise in Covid-19 cases and hospitalizations. Some analysts have argued over whether these various hotspots amount to a “secondary spike” in the US when many of these states never suffered a significant initial surge like New York, New Jersey, Washington, and elsewhere. Also, there remains uncertainty over the degree to which this apparent increase in cases might be attributable to more widespread testing rather than a true uptrend in new infections. New York Governor Cuomo issued a warning over the weekend that he will seek to shut businesses that are flouting the mandated precautions for safe reopening. Meanwhile, Beijing is also experiencing a targeted lockdown after a resurgence in infections centered around a seafood and produce market has been the source of new coronavirus cases in half the districts of the city. For context, reports indicate that life in Beijing had returned to relative normalcy in recent weeks after a 50-day period without any new reported cases. –

Chinese Data Suggests a Tepid Rebound

Despite being further along the timeline of pandemic containment and economic reopening, China’s economic data continues to suggest lingering effects of the virus. Overnight, China’s key growth readings for May generally undershot estimates and conveyed a picture of gradual resumption of economic activity rather than the V-shaped rebound that some analysts had hoped. Retail sales were -2.8% year-on-year (y/y), missing expectations of -2.3% but improving from April’s contraction of 7.5%. Industrial production registered an expansion of 4.4% y/y, accelerating from the prior month’s 3.9% growth but was still shy of the forecast pace of 5.0%. Fixed asset investment, which is quoted on a year-to-date basis, slightly topped estimates, posting -0.3% versus -0.8% consensus expectations and -3.3% in April. Commentators are citing weak demand, both domestically and overseas, for the halting progress in China’s economic recovery even months past the peak of the pandemic on the mainland. Meanwhile, the Trump administration continues to send upbeat signals on the recovery, with National Economic Council (NEC) Director Kudlow stating yesterday that he sees a “very good chance” of the US economy experiencing a V-shaped rebound over the second half of this year. Last week, the Fed’s updated projections for growth in 2020 and 2021 were consistent with lingering headwinds from the pandemic. The OECD and World Bank also issued downgraded forecasts last week and the IMF is set to follow suit.

Additional Themes

White House Officials Discuss Upcoming Stimulus Measures – Over the weekend, White House advisor Navarro indicated that President Trump is seeking at least $2 trillion for the next pandemic relief bill, which administration officials have suggested would be delayed until late July. This contrasts with the statements of Senate Majority Leader McConnell, who has stated that this next fiscal package should be closer to $1 trillion. Navarro also noted the continued White House preference for a payroll tax cut. Meanwhile, NEC Director Kudlow indicated that the White House remains committed to the end-July expiry of augmented unemployment benefits, as they represent a “disincentive” to return to work. Administration officials and GOP Senators have proposed instead a “back to work” bonus for employees.

Flaring Tensions on Korean Peninsula – Increasingly bellicose rhetoric from North Korea has featured threats to cut off communications as well as aggressive pronouncements from Kim Jong Un’s sister, who analysts speculate may be the leading candidate to succeed her brother as questions continue to swirl over his health. The South Korean government called an emergency session on Sunday to assess the situation. South Korean assets, which tend to be resilient in the face of North Korean bluster, underperformed significantly overnight, with the Kospi retreating 4.8% and the Korean won sinking 1.0% versus the dollar.

Summary and Price Action Rundown

Global risk assets staging a rebound that is set to retrace a portion of yesterday’s major downside, as investors grapple with the risk that a secondary spike in US Covid-19 infections will impede economic reopening. S&P 500 futures point to a 1.6% higher open after the index suffering its worst single-session loss since March, plummeting 5.9% yesterday. This brought total losses over the past three sessions to 7.1% after Monday’s gain erased all of the S&P 500’s year-to-date downside. The Nasdaq sank 5.3% yesterday after registering a new record high the day before. Equities in the EU are similarly rebounding while Asian stocks posted moderate declines overnight. Longer-dated Treasury yields have stabilized after a round-trip over the past week, with the 10-year yield climbing back to 0.71% this morning, while the dollar is also steadying after yesterday’s burst of appreciation. Crude oil is flat, with Brent below $39.

Market Volatility Re-Intensifies Abruptly

After weeks of unrelenting equity upside premised on hopes of a swift recovery in economic activity, with tailwinds from vaccine hopes and magnanimous Federal Reserve liquidity, the upbeat trends reversed sharply yesterday amid resurgent doubts over the outlook for reopening. Analysts are pointing to various downside catalysts for yesterday’s dramatic return of volatility in stocks and global risk assets generally, chief among them the troubling data on re-intensifying Covid-19 infections in various US regions and cities that have been in the process of reopening for economic activity. Amid a resurgence of coronavirus infections, reports indicated that Houston may reopen its emergency medical facilities housed at NRG Stadium while Nashville announced a delay in its reopening plans. The downbeat tone and grim outlook communicated by the Federal Reserve at their June meeting earlier this week has also been cited as weighing on sentiment. However, this cautious messaging from Chair Powell and his FOMC colleagues has been broadly consistent for months, with the updated forecasts only adding a degree of specificity to their concerns. Lastly, the astounding speed and magnitude of the runup in equities is another factor that market participants are noting, with a technical pullback long overdue after the dizzying climb from the low of March. For context, the Nasdaq broke to new record highs on Wednesday and the S&P 500 had erased all of its 2020 downside on Monday’s rally. These stunning rebounds have placed US stocks at significantly higher valuations than earlier in the year given the impaired earnings outlook.

Trump Administration Holds the Line on Reopening and Delayed Fiscal Stimulus

Treasury Secretary Mnuchin echoed President Trump’s various pronouncements on the shifting White House policy stance toward Covid-19 yesterday, indicating that the US should not resort to lockdowns again and that another pandemic relief bill will be delayed until later in the summer. In remarks on CNBC yesterday, Treasury Secretary Steven stated that the US should not shut down the economy again even if there is a resurgence in coronavirus cases. He defended this position, which President Trump has recently espoused, by expressing confidence in the nation’s Covid-19 testing abilities, improved contact tracing, and general knowledge on the virus. Thus, Mnuchin stated, “it will not be necessary to impose restrictions again…We’ve learned that if you shut down the economy, you’re going to create more damage.” Additionally, Mnuchin applauded the bipartisan efforts to bring $6 trillion in stimulus to the economy, but he reiterated the Trump administration’s resistance to expediting another stimulus bill, preferring instead to wait until after July to negotiate the finer details of the next package. Senate Republicans have been pushing firmly for this hiatus in relief spending. “One of the things we’re going to need to be focused on is how do we help the industries that are especially impacted: hotel, travel, entertainment, restaurants,” Mnuchin said.

Additional Themes

UK Economy Contracts Sharply in April – The monthly economic GDP reading for the UK posted a 20.4% retrenchment in April from March, which had also been in negative territory but to a shallower degree at -5.8% month-on-month (m/m). Reports indicated that not only was April the sharpest UK GDP decline on record but it erased 18 years of economic expansion, shrinking the economy back to the size it was in 2002. Still, this brutal statistic was only moderately worse than the consensus forecast of -18.7% m/m and took the three-month rate to -10.4%. Industrial and manufacturing production figures for April were similarly dire. For context, the UK has the highest Covid-19 mortality rate in Europe and is facing the prospect of a no-deal Brexit at year-end. Nevertheless, the pound is steady today, holding near its highest level versus the dollar since mid-March, indicating that market participants remain focused on the recovery.

Looking Ahead – The Bank of England meets next week amid the dismal UK data, with some analysts predicting a rate cut to 0%. The Bank of Japan also has a meeting. US retail sales and industrial production for May will be in focus along with more weekly jobless claims

Summary and Price Action Rundown

Global risk assets are moving lower this morning as the cautious tone of yesterday’s Federal Reserve communications and signs of a potential secondary spike in US Covid-19 infection data raise concerns that recovery optimism had become overdone in recent weeks. S&P 500 futures indicate a -1.7% lower open after the index erased all of its year-to-date downside on Monday and then posted two consecutive days of losses for the first time in nearly a month. The Nasdaq is also set to open to losses after registering a new record high yesterday. Equities in the EU and Asia also retreated overnight. Longer-dated Treasury yields have almost fully reversed last week’s breakout from their two-month trading range, with the 10-year yield descending to 0.71% this morning, while the dollar is receiving a renewed safe-haven bid after falling steeply over recent weeks. Crude oil is lower as well, with Brent slipping below $41.

Fed Holds Policy Steady and Commits to Extend Extraordinary Easing

Yesterday, the FOMC retained its current policy settings and Chair Powell discussed the potential for yield caps and augmented guidance down the road as expected, though some analysts are pointing to the Fed’s focus on downside risks as denting market sentiment. The highly anticipated FOMC decision yesterday matched consensus expectations that rates would be left unchanged and no new policies would be enacted. Still, the tone of the accompanying statement and Chair Powell’s press conference was decidedly cautious, which is consistent with prior communications. According to the updated interest rate projections (the “dot plot”), all but two FOMC members expect that it will be appropriate to keep rates at zero through 2022. However, market participants were left uncertain regarding future policy maneuvers, with Chair Powell again only noting that forward guidance and yield curve control (YCC) are being considered. Alongside the rate outlook, the Fed projected that the US economy will shrink 6.5% in 2020 but show a 5.0% gain in 2021 followed by 3.5% in 2022, with unemployment estimated to be 5.5% by the end of 2022. The range of forecasts is wide, however, reflecting great uncertainty over the possible lingering impact of the virus. Also, the Fed reinforced its commitment to maintain “smooth market functioning” by promising to maintain its Treasury and mortgage purchases “at least at the current pace” of $80bn Treasuries and $40bn of mortgage backed securities (MBS) a month “over coming months,” as opposed to its previously open-ended commitment to quantitative easing (QE). For context, the Fed went from a peak of $300 billion a month in Treasuries during the early days of the coronavirus crisis to $80 billion more recently. The QE outlook seems to have been somewhat below consensus expectations, with some market participants anticipating an increase in Treasury purchases and doubling of MBS purchases. The stock market reaction was initially mixed, as growth-sensitive equity sectors retreated and tech stocks surged anew, but sentiment has turned more negative overnight. Meanwhile, the ensuing downside for Treasury yields and the dollar is straightforward and consistent with the exceptionally dovish rate messaging.

Covid-19 Conference Call on Resurgence Risk

The rising potential for a secondary spike of Covid-19 cases as lockdowns ease is another factor that is weighing on investor sentiment this week. Analysts continue to monitor figures showing an increase in coronavirus cases in California, Florida, Texas, Arizona, other states that have been in the process of reopening for economic activity. Yesterday, Texas reported its highest number of daily cases since the pandemic began. White House public health advisor Dr. Fauci stressed in remarks earlier this week that the coronavirus pandemic “isn’t over yet” in the absence of a vaccine. – MPP conference call: Please join us this morning at 11am for a call with Dr. Chris Mores, a virologist and Program Director for the Global Health Epidemiology and Disease Control MPH program at the Milken Institute School of Public Health of George Washington University. Dr. Mores will discuss how he is interpreting the latest Covid-19 infection data and his outlook for the coming months, particularly in light of the mass gatherings in many US cities over the past week.

Dial-in Details:

Dial-in number (US): (351) 888-7930

International dial-in numbers: https://fccdl.in/i/brendanwalsh

Online meeting ID: brendanwalsh

Join the online meeting: https://join.freeconferencecall.com/brendanwalsh

Additional Themes

US Jobless Data in Focus After Nonfarm Payroll Surprise – Initial unemployment claims for the week ending June 6th are expected to show 1.550 million new filings. For context, the prior week, 1.877 million Americans filled for unemployment benefits, the lowest level since the coronavirus crisis began almost three months ago. Still, this was slightly above market expectations of 1.80 million and lifted the total reported since March 21st to 42.6 million. The largest increases in jobless claims were reported in California and Florida, while those in New York dropped sharply. Meanwhile, continuing claims unexpectedly rose to 21.5 million in the week ended May 23rd, above expectations of 20 million. These datapoints contrast with last Friday’s May nonfarm payroll data, which showed that the US economy gained 2.5 million jobs in May, smashing expectations of 7.5 million more jobs lost and marking the largest jobs increase in the history of the series after 20.7 million lost jobs in April.

Crude Prices Retreat from Recent Highs – US crude inventories hit a record high last week after posting declines for three of the four preceding weeks, compounding pressure on oil prices as traders increasingly question the optimistic case for a rebound in

Summary and Price Action Rundown

Global risk assets are fluctuating moderately this morning ahead of today’s Federal Reserve decision, while investors continue to monitor noisy economic data for signs of a rebound alongside Covid-19 infection data for the risk of a secondary spike. S&P 500 futures point to a flat open after the index backed off its loftiest level since late February yesterday following a dizzying two-week surge higher. Equities in the EU and Asia similarly lacked direction overnight. Longer-dated Treasury yields continue to retrace last week’s breakout from their two-month trading range, with the 10-year yield descending to 0.80%, while the dollar struggles amid anticipation of more ultra-accommodative messaging from the Fed today. Crude oil remains choppy at current levels, with concerns over today’s US stockpile figures weighing this morning.

Investors Await Today’s Conclusion of the June Federal Reserve Meeting

Significant monetary policy changes are not expected, so the focus will be on the accompanying communications, which will include new economic and interest rate projections. In his press conference following today’s FOMC decision, Chair Powell is expected to discuss additional policy options to extend their extraordinary monetary easing over the coming quarters, with yield curve control and enhanced forward guidance sure to be among the options discussed. Analysts will be attuned to the Fed’s treatment of last week’s spike in nonfarm payrolls for May given that FOMC members have been almost entirely focused on downside risks to the economy in their remarks over the past weeks and months. There will also be scrutiny of the Fed’s quasi-fiscal programs that are designed to provide funding to corporations, states and municipalities, and medium-sized businesses. Earlier this week, the Fed announced yesterday afternoon that it would be adding further flexibility to the terms of its long-awaited Main Street Lending program, cutting the minimum loan size to $250k from $500k, allowing a deferral of principal repayments for up to two years instead of the previous one-year grace period, and lengthening the maturity from four years to five. Chair Powell is likely to be pressed for further details on the timeline for launch of this program. This meeting also will include new FOMC economic projections and the dot plot of expected rate levels, as well as a focus on the risks of self-reinforcing disinflationary dynamics (more below).

Global Economic Data Remains Inconclusive on Recovery Trajectory

Despite euphoria in equities and incrementally encouraging signs from other financial markets, last Friday’s astoundingly upbeat nonfarm payroll numbers remain the exception amid uneven and fitful signals from most other traditional economic data. After the World Bank’s dismal projections earlier this week, the OECD weighed in with its forecasts for a 6% global growth contraction this year, with its estimate for US GDP at -7% and the EU at -9%, and only a 5% rebound in 2021 for the worldwide economy. Overnight, South Korea, which is held as the gold standard in Covid-19 containment for a major sovereign nation, reported its highest level of unemployment in a decade in May despite social distancing restrictions having been lifted in April. Joblessness rose to 4.5% from 3.8% the prior month, outpacing expectations for an increase to 4.0%. Economists cite the lack of external demand as continuing to weigh on the trade-oriented South Korean economy. Meanwhile, data filtering in from April continues to show the depths of the economic shock from the pandemic, with Japan machine tool orders contracting 12.0% month-on-month while Germany’s exports plunged 24.0% month-on-month and 31.1% year-on-year, sending the trade surplus to its steepest monthly decline on record and the narrowest point since December 2000.

Additional Themes

Deflation Risks in Focus – Overnight, releases of May producer price data in Japan and China showed worsening deflationary pressures, with respective readings of -2.7% year-on-year (y/y) and -3.7% y/y both undershooting estimates and evidencing deterioration from April’s level. In the US, May consumer goods inflation data is out today, and the producer price index is due tomorrow, with expectations for stabilization of both gauges. Market-based indicators of long-run inflation expectations for the US, such as 10-year TIPS breakevens, have rebounded from the March trough but only to equal the previous multi-year lows of the 2016 global deflation scare.

Wariness Continues over Coronavirus Data – Analysts continue to monitor figures showing an increase in Covid-19 cases in California, Florida, Texas, Arizona, other states that have been in the process of reopening for economic activity. Reports yesterday also indicated that a number of National Guardsmen mobilized to respond to protests last week have tested positive for Covid-19. White House public health advisor Dr. Fauci stressed in remarks yesterday that the coronavirus pandemic “isn’t over yet” in the absence of a vaccine.

Summary and Price Action Rundown

Global risk assets are moving lower this morning as the dizzying rally fueled by optimism over economic reopening takes a breather, with investors weighing the latest Covid-19 data and looking ahead to this week’s Federal Reserve meeting. S&P 500 futures point to a 0.8% lower open after the index erased its 2020 losses yesterday following a two-week sprint higher during which it gained 9.4% over 10 trading sessions. The S&P 500 is now barely 4% below record highs from February while the tech-heavy Nasdaq registered a new record high and is up 12.7% year-to-date. Equities in the EU are also retracing a portion of their ongoing rally this morning, while Asian stocks were mixed overnight. Longer-dated Treasury yields are unwinding their breakout from their two-month trading range, with the 10-year yield settling to 0.83%, while the dollar is pausing its downtrend. Crude oil is also in counter-trend mode this morning after climbing briefly to a new multi-month high yesterday on the OPEC+ supply cut extension.

Markets Pause to Assess Reopening and Recovery Prospects

Amid mixed signals from financial markets, public health officials, economic data, and Covid-19 infection figures, investors are pondering whether the recent bout of optimism has been overdone. The sense of relief in recent weeks has been palpable, with even the US epicenter of the pandemic, New York City, starting the process of reopening this week after two months of lockdown. According to the NYC Department of Small Business Services, about 16,000 “nonessential” retail businesses and 3,700 manufacturing companies will reopen, in addition to more than 32,000 construction sites being allowed to restart work. Absent a resurgence of cases, the city could move into the second phase of reopening after two weeks. A gauge of US small business optimism released this morning captured the hopeful mood, rising to 94.4 in May from 90.9 the prior month, though the uncertainty subcomponent remains elevated. Some Congressional Republicans are seizing on the improving outlook, most prominently featured in the May nonfarm payroll spike, to advocate for a longer pause before passing the next pandemic relief bill. White House advisor Kevin Hassett said yesterday that the odds of another aid package were “100%” but suggested that the Trump administration would prefer to see July data before deciding on the magnitude and substance of the bill. Meanwhile, analysts are monitoring data showing an increase in Covid-19 cases in California, Florida, Texas, other states that have been in the process of reopening, though increased testing may be a factor.

Federal Reserve Tweaks Lending Program Ahead of June Meeting

Monetary policy is in the spotlight this week as the FOMC begins its two-day meeting today. In advance of its June meeting, the Fed announced yesterday afternoon that it would be adding further flexibility to the terms of its Main Street Lending program, cutting the minimum loan size to $250k from $500k, allowing a deferral of principal repayments for up to two years instead of the previous one-year grace period, and lengthening the maturity from four years to five. This comes as market participants await what is expected to be a relatively uneventful FOMC meeting from a policy perspective, with all settings expected to remain steady, but with significant interest as to the accompanying communications on future monetary maneuvers. Specifically, Chair Powell is expected to discuss additional policy options to extend their extraordinary monetary easing over the coming quarters, with yield curve control and enhanced forward guidance sure to be among the options discussed. This meeting also will include new FOMC Economic Projections and the dot plot of expected rate levels.

Additional Themes

Oil Prices Stumble on Saudi Announcement – Crude oil is continuing to retrace a portion of its steep multi-month rally as traders take profits after OPEC and its allies (collectively known as OPEC+) agreed on Saturday to extend output curbs through July. Notably, however, Saudi’s Energy Minister announced that the Kingdom’s voluntary additional cuts of 1.2 million barrels per day will conclude in June, weighing further on oil prices yesterday. Other headwinds include the resurgence of Libyan output and a burgeoning recovery in US shale oil production.

World Bank Issues Grim Outlook – Amid the global economic fallout from the coronavirus pandemic, emerging and developing economies are set to shrink this year for the first time in the last 60 years according to the World Bank. The bank’s forecast warns that as many as 100 million people in the developing world will be tipped into extreme poverty by a projected 2.5% contraction in emerging markets’ GDP. Recently, major developing countries have seen a rapid increase in Covid-19 cases, including Brazil, Russia, and India. Overall, the World Bank sees the global economy shrinking 5.2% for the year, which is steeper than the IMF’s -3.0% projection from April, reflecting the growing economic impact of the virus. The report warned of a more adverse scenario in which the global GDP contraction could be as high as 8%, with emerging market economies shrinking around 5% and an estimated sluggish 1% global recovery in 2021.

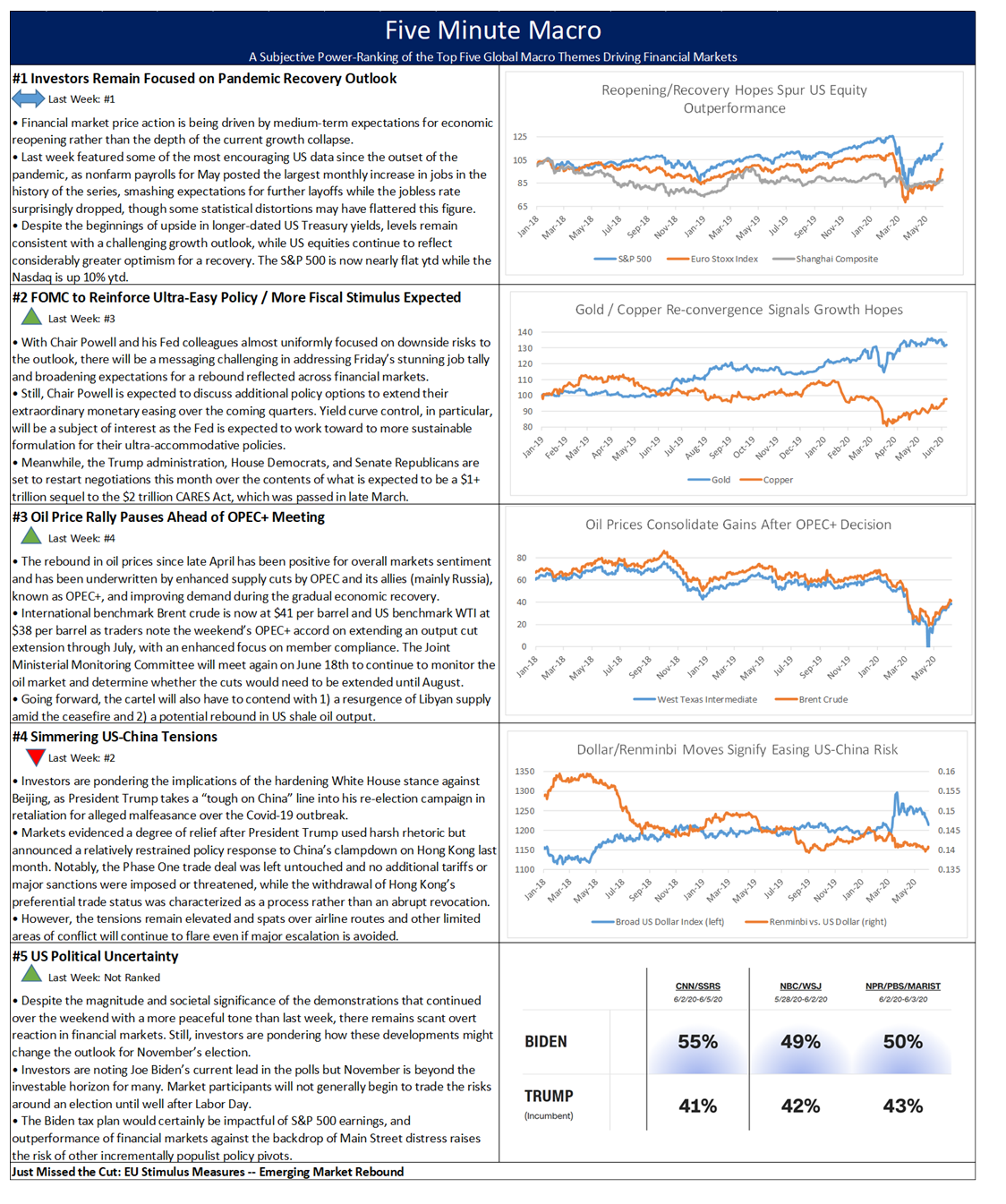

Pandemic recovery remains the main driver of markets, while aggressive Fed stimulus comes in second. The rally in oil moves into the third spot, with China/US tensions dropping down a few spots. Finally, US political uncertainty enters the top five.

Summary and Price Action Rundown

Global risk assets are mostly higher this morning amid continued optimism over economic reopening, rising oil prices following the OPEC+ agreement, and expectations for more exceptionally accommodative messaging from the Federal Reserve at this week’s meeting. S&P 500 futures indicate a 0.4% higher open, which would add to last week’s torrid 4.9% gain that cut year-to-date downside to a mere 1.4% and the decline from February’s record high to 5.7%. Equities in the EU are retracing a portion of their ongoing rally this morning, while Asian stocks also posted gains overnight. Longer-dated Treasury yields are extending their breakout from their two-month trading range, with the 10-year yield rising to 0.91%, while the dollar is continuing its downtrend. Crude oil is climbing to a new multi-month high after OPEC and its allies agreed over the weekend to extend supply cuts (more below).

OPEC+ Unites Over Further Supply Cuts

Crude oil is continuing its steep multi-month rally after OPEC and its allies (collectively known as OPEC+) agreed on Saturday to extend output curbs through July with a focus on stricter compliance. Key aspects of the deal include an agreed-upon 9.6 million barrels per day (bpd) cut through July (slightly lower than previous 9.7 million bpd due to Mexico’s withdrawal from supply cuts) and previously non-compliant countries from May and June making extra supply reductions to compensate, a point that was non-negotiable to both Saudi and Russian officials. These compensatory measures will turn investor attention towards the compliance of Iraq and Nigeria over the next few months as the primary indicator of the cohesiveness of the cartel’s agreement. The Joint Ministerial Monitoring Committee will meet again on June 18th to continue to monitor the oil market and determine whether the cuts would need to be extended until August. Going forward, the cartel will also have to contend with two key factors that may work to counter their efforts to support prices. First is the resurgence of Libyan oil, as the ceasefire agreement has already seen the resumption of production at the war-torn country’s largest oil facilities. Second is the potential rebound in US shale oil output, with reports noting that producers are starting to undo the shut-ins that have occurred over the past few months.

Economic Data Sends Mixed Signals Over Global Recovery

As analysts continue to ponder the dramatic upside surprise in last Friday’s US nonfarm payroll figures for May, data from overseas suggests that the recovery remains fitful. Although April data may be considered somewhat stale and backward-looking, German industrial product for the month was worse than anticipated, contracting 17.9% month-on-month and 25.3% year-on-year (y/y). Automobile sales in Germany were down 50% y/y in May, though China’s car buying rebounded for a gain of 1.9% y/y. Not all the data from China was positive, however, with May exports down -3.3% y/y and imports -16.7% y/y, with the former moderately better than expected but the latter considerably weaker. However, analysts noted that the import data showed large increases in crude oil and soybean purchases, which are suggestive of compliance with Phase One trade deal commitments. Meanwhile, Japan’s revised first quarter GDP figure showed an improvement from the initial reading of -3.4% quarter-on-quarter annualized contraction to 2.2%, though economists are pointing to possible distortions in the figure based on challenging reporting conditions during the onset of the pandemic. Similarly, market participants are trying to parse the significance of the “misclassification error” disclosed by the Bureau of Labor Statistics, which led to a significant understatement of the unemployment rate in Friday’s stunning release. For context, the unemployment rate fell to 13.3% after record highs in April, well below market expectations of 19.8%. The number of unemployed persons fell by 2.1 million to 21 million. However, the real unemployment rate is another 3% higher at 16.1% due to continued misclassifications in BLS household surveys regarding temporary layoffs due to the pandemic. The challenge is the treatment of furloughed workers, who reported that they remain employed but absent at the direction of management.

Additional Themes

US Protests Remain a Backburner Issue for Markets – Despite the magnitude and societal significance of the demonstrations that continued over the weekend with a more peaceful tone than last week, there remains scant overt reaction in financial markets. Still, investors are pondering how these developments might change the outlook for November’s election.

This Week – Analysts will be highly attuned to how Chair Powell and the FOMC frame the surge in May nonfarm payrolls on Wednesday at the conclusion of the two-day Fed meeting. Aside from the FOMC, this week’s calendar is somewhat light. Initial jobless claims and continuing jobless claims will be in focus on Thursday. Consumer and producer price indexes will be noted, but are unlikely to move the market, while the consumer sentiment gauge on Friday will be salient to the assessment of the ongoing economic rebound.

Summary and Price Action Rundown

Global risk assets are advancing this morning amid expectations for better-than-feared US labor market and an impending OPEC agreement to extend price-supportive supply cuts. S&P 500 futures point to a 0.8% higher open, which would add to week-to-date gains of 2.2% that have reduced year-to-date downside to 3.7% and the decline from February’s record high to 8.1%. Equities in the EU are soaring after a week of massive fiscal and monetary stimulus in the bloc, while Asian stocks also posted gains overnight. Longer-dated Treasury yields are extending their breakout from their two-month trading range, with the 10-year yield rising to 0.87% even before the nonfarm payroll data is out, while the dollar remains in a steep downtrend. Crude oil is jumping to a new multi-month high as OPEC prepares to extend supply cuts (more below).

Recovery Hopes Build to a Crescendo Ahead of Nonfarm Payrolls

After yesterday’s somewhat disappointing jobless claims figures contrasted with the more upbeat ADP payroll estimates earlier this week, markets are poised for a positive signal from this morning’s May nonfarm payroll numbers. Later this morning, the BLS will release the official May Employment Report, where expectations are for 7.5 million job losses and an unemployment rate of 19.1%. Markets are leaning toward a better-than-expected release, however, with the 10-year Treasury yield breaking to its highest level since late March and US equity futures soaring ahead of the open. For context, the US economy lost 20.5 million jobs in April, better than consensus estimates of 22 million, which followed 870K losses in March. April’s tally was the largest monthly decline in US employment ever recorded, and the unemployment rate jumped to 14.7%, the highest in the history of the series but still below consensus expectations of 16%. The number of unemployed persons rose by 15.9 million to 23.1 million. However, the real rate is another 5% higher, as the BLS does not include people who are not looking for a job as unemployed. 18.1 million of the newly unemployed characterized themselves as only temporarily laid off and expect to return to work once restrictions are loosened. The labor force participation rate decreased by 2.5% points to 60.2%, the lowest rate since January 1973. Earlier this week, labor market data has conveyed some mixed signals. Thursday’s release showed that 1.9 million Americans filed for unemployment benefits last week, the lowest amount since the coronavirus crisis began, but slightly above market expectations of 1.8 million. This puts the total reported since March 21st at 42.6 million. Meanwhile, continuing claims unexpectedly rose to 21.5 million in the week ended May 23rd, above expectations of 20 million. On the brighter side, payroll company ADP estimated that in May private businesses laid off 2.8 million workers, after shedding a downwardly revised 19.6 million in April, which was much better than market forecasts of a 9.0 million job loss.

OPEC Goes Back to the Negotiating Table

Oil prices are advancing this morning as OPEC and its allies (collectively known as OPEC+) have agreed to meet tomorrow to agree on an extension of ongoing supply reduction agreements. For context, oil prices had retreated from multi-month highs earlier this week as OPEC+ and its allies looked set to push their June meeting back for weeks over issues of noncompliance with ongoing production cut commitments, with Nigeria and Iraq meeting less than half the cuts necessary in May. The energy ministers of the delinquent cartel members reconfirmed their quota commitments on Tuesday, however, and Russia and Saudi subsequently affirmed their tentative agreement to extend current supply cut levels of 9.7 million barrels per day through July, putting a floor under crude prices. In addition to cartel supply cuts, the continued oil uptrend over the past month has been underwritten by resumed economic activity in China, the slow lifting of lockdown measures worldwide, and declining production from the US shale patch. Yesterday, the Energy Information Administration reported a 2.1 million barrel decrease in US stockpiles from last week. Brent crude has now retraced nearly half of its 2020 decline from $69 per barrel in January down to $19 in April.

Additional Themes

Air Travel Remains a US-China Sticking Point – US airlines rebuffed China’s announcement earlier this week that it would begin lifting restrictions on foreign carries beginning Monday, calling it a step in the right direction but insufficient to address their concerns. News on Wednesday afternoon that the US would block Chinese airlines in a tit-for-tat exchange for China’s restrictions on US carriers was largely overlooked by market participants, who have dialed back concerns of a significant rupture in US-China relations.

PPP Revisions Pass the Senate – Yesterday, the Senate passed legislation that will allow small businesses more flexibility in using the rescue-loan funds from the Paycheck Protection Program (PPP). This comes as Congress and the Trump administration prepare to negotiate the next round of fiscal spending to cushion the economic blow of the pandemic.

Summary and Price Action Rundown

Global risk assets are pausing for breath this morning after a brisk multi-week rally as investors await today’s European Central Bank decision and key US economic data. S&P 500 futures indicate a 0.5% lower open, which would pare week-to-date gains of 2.6% that has narrowed the index’s year-to-date downside to 3.3% and the decline from February’s record high to 7.8%. Equities in the EU moderately lower while Asian stocks were mixed overnight. Longer-dated Treasury yields are steady near the top of their range, with the 10-year yield at 0.74%. Meanwhile, the dollar is retracing a portion of its recent decline as the euro gives back some of its rally, though the renminbi was steady overnight. Crude oil is falling further below its recent multi-month high as OPEC struggles to extend supply cuts (more below).

EU Asset Rally Pauses Ahead of the ECB

European assets are consolidating a portion of their recent and substantial gains as investors await a key decision by the European Central Bank (ECB) later this morning. At 7:45am ET, the ECB will issue its much-anticipated decision for its June meeting. Growth prospects for the euro area are grim, and the ECB expects a 5%-12% GDP contraction this year. Still the ECB is expected to leave interest rates unchanged as it did at its April meeting, holding the main refinancing rate at 0% and its deposit interest rate at -0.5%. Instead, the ECB is widely expected to expand its Pandemic Emergency Purchase Program (PEPP) and estimates for the upsizing range between €500 billion and €750 billion alongside expectations for extension to year-end. This could be the extent of what the ECB can do unilaterally in terms of asset purchases, given rising German opposition, without rallying support from national governments for further action. Meanwhile, overnight, German Chancellor Merkel secured agreement for additional fiscal support for the EU’s largest economy worth €130 billion, though direct support for the German auto industry through cash incentives to purchase cars was not included in the final version. Shares of German automakers are retracing a portion of their recent rally this morning, declining between 2% and 4%. This comes as the bloc continues to negotiate a draft for a €750 billion pan-EU pandemic relief budget that represents a vital step towards fiscal unionization and is based on a Franco-German plan released on May 18th. Since that date, the Euro Stoxx index is up 17.3%, outpacing the 9.1% gain for the S&P 500 over that period, while the euro is 3.6% stronger versus the dollar and the yields on peripheral EU debt, like Italian and Spanish bonds, have converged swiftly toward German bund yields. Though EU risk assets have begun to reflect a more upbeat view of the recovery amid the ample stimulus, regional economic data remains deeply depressed. April retail sales registered -19.6% year-on-year, only slightly better than estimates of -20.6% and down from the prior month’s -8.8% pace of contraction.

Investors Await Further Signs of Improvement in US Data

With growing signs of recovery in May helping fuel US stock market euphoria over the prospect of a solid summer growth rebound, today’s weekly jobless data is expected to show continued easing in layoffs. For the week ending May 30th, economists estimate that initial jobless claims will decline to 1.8 million from the prior week’s tally of 2.1 million new filings, which would mark a new weekly low since the coronavirus crisis began. Improvement aside, these tallies are grim, and the total of new unemployment benefits reported since March 21st is set to rise above 42 million. However, the continuing jobless claims decreased by 3.9 million to 21.1 million in the week ended May 16th from a record 24.9 million in the week ended May 9th. This is an indication that as states lifted stay at home orders, the process of returning to work has slowly begun. Today’s data for the week ending May 23rd is expected to show a further decline to 20.0 million, though reporting issues, particularly in California and Florida, may be skewing these numbers. For context, yesterday featured some relatively upbeat jobs data as payroll company ADP estimated that in May private businesses laid off 2.8 million workers, after shedding a downwardly revised 19.6 million in April, which was much better than market forecasts of a 9.0 million job loss. On Friday, the BLS will release the official May Employment Report, where expectations are for 8.0 million job losses and an Unemployment Rate of 19.8%.

Additional Themes

China Moves on Air Travel – News yesterday afternoon that the US would block Chinese airlines in a tit-for-tat exchange for China’s restrictions on US carriers was largely overlooked by market participants, who have dialed back concerns of a significant rupture in US-China relations after President Trump’s restrained reaction to the situation in Hong Kong. China announced overnight that it would lift restrictions on foreign carries beginning next week.

OPEC Meeting Pushed – Crude oil prices are stumbling below multi-month highs as this week’s OPEC+ meeting looks set to slide to mid-month amid drama over supply cut non-compliance by Iraq and others. Russia and Saudi Arabia are said to demand full adherence before the meeting.