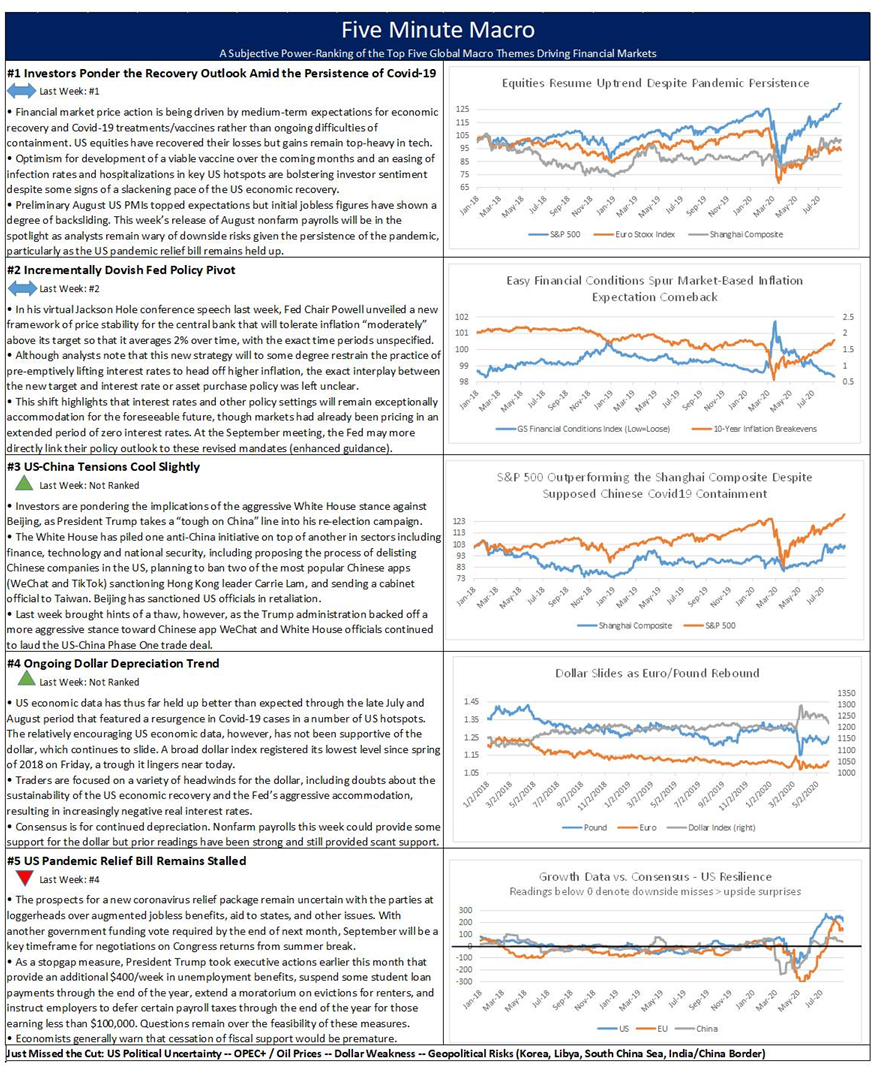

Summary and Price Action Rundown

Global risk assets are attempting to stage a rebound from yesterday’s renewed selloff this morning as equity price action remains choppy, while investors continue to monitor currency messaging by the European Central Bank and fiscal stimulus prospects in the US. S&P 500 futures point to a 0.8% higher open after the index fell 1.8% yesterday, retracing most of Wednesday’s rebound to pare its year-to-date upside to 3.4%, which is nearly 7% below last Wednesday’s record high. The tech-heavy Nasdaq has reverted to its recent underperformance trend, falling 2.0% yesterday to shave its robust year-to-date gains to 21.7%. Equities in the EU are flat this morning while Asian stocks were mostly higher overnight. A broad dollar index is turning back toward its recent 28-month low, while longer-dated Treasury yields are rangebound, with the 10-year yield at 0.69%. Brent crude prices are hovering below $40.

ECB Officials Continue to Refine Messaging on the Euro

The European Central Bank (ECB) Chief Economist has reemphasized currency strength as a headwind to reflation in the EU after yesterday’s policy meeting sent mixed messages on the currency. Earlier today, Chief Economist Lane tweeted his assessment that the ongoing appreciation of the euro has “significantly muted” inflationary pressures in the EU, seemingly taking a more forceful stance on the currency than ECB President Lagarde expressed in her post-meeting remarks yesterday. For context, Lane first emphasized euro appreciation as a headwind to reinflation on September 1st, just as the single currency was nearing the closely-watched level of $1.20, which is more than a two year high. From its March lows, the euro has gained more than 10% against the dollar and inflation is set to be negative for the first time in four years. Lane’s strong emphasis on the link between currency strength and disinflation contrasts with President Lagarde’s more tepid statement yesterday that “clearly to the extent that the appreciation of the euro puts negative pressure on prices, we have to monitor carefully such a matter, and this was extensively discussed.” Then she stressed that the ECB does not target the exchange rate and will likely not adopt a targeting strategy, though it remains cognizant of its movements. The euro moved higher during the ECB meeting, gaining nearly 1% versus the dollar before settling back in later trading, but is now moving higher again. Analysts cite continued strength in the euro as a potential catalyst, among a resurgence of Covid-19 and backsliding inflation metrics, as the likely catalysts for the ECB to expand the €1.35 trillion Pandemic Emergency Purchase Program (PEPP) as early as the December meeting.

Questions Linger Over the US Rebound as Stimulus Negotiations Sputter

The negotiations over the latest pandemic stimulus remain in limbo after yesterday’s failure of Senate Republicans’ “skinny” version of the bill, while recent US economic data has shown some hints of further backsliding. Recent US labor market data, in particular, has been somewhat mixed. Yesterday’s release of initial jobless claims for the week of September 5th registered a modest disappointment, remaining unchanged at 884K and missing market expectations of 850K, while continuing claims for the prior week rose nearly 100K to 13.38 million, also above expectations of 12.904 million. Alongside the disappointing initial claims, claims for Pandemic Unemployment Assistance (PUA) rose by 91K, marking the fourth straight increase. Combining the standard claims with PUA continuing claims means that 27.8 million people are receiving unemployment insurance payments, up from 25.7 mil in early August. For context, the Labor Department changed the seasonal adjustment procedure last week that flattered the headline initial claims figure, which would have been over 1 million using the prior formulation. This comes as the prospects for additional fiscal support continue to darken. The latest iteration of the pandemic relief bill, a roughly $500 billion package crafted by Senate Republican, failed in a procedural vote broadly along party lines yesterday. Senate Majority Leader McConnell has accused the Democrats of stonewalling for political gain while Senator Schumer expressed hope that blockage of the so-called “skinny” bill could entice Senate Republicans and the White House back to negotiations.

Additional Themes

TikTok Deadline Reaffirmed – President Trump has stated that his deadline for arranging a sale of the controversial Chinese app’s US operations before his ban on its use takes effect will not be extended. Regarding the timing, September 15th has been the stated deadline, though some analysts suggest that the actual deadline is September 20th, which is when the ban would become official. With Microsoft and Oracle among the suitors for the social media platform’s US operations, and Beijing likening the process to theft and asserting its right to veto any potential deal, this episode has become a focal point of US-China friction in recent months. Yesterday, reports emerged that the Chinese owner of TikTok, ByteDance, was in talks with US government officials in an effort to continue US operations absent a complete sale of the business, though it was not clear how data security could be assured in such an arrangement.

Looking Ahead – Next week’s calendar features a Fed meeting, as well as decisions from the Bank of England and Bank of Japan. Japan’s ruling party will also vote on the successor to outgoing Prime Minister Abe. US retail sales and industrial production data for August will be in the spotlight, alongside another weekly initial jobless claims tally, while China and the EU will also be issuing key industrial and consumer data for last month