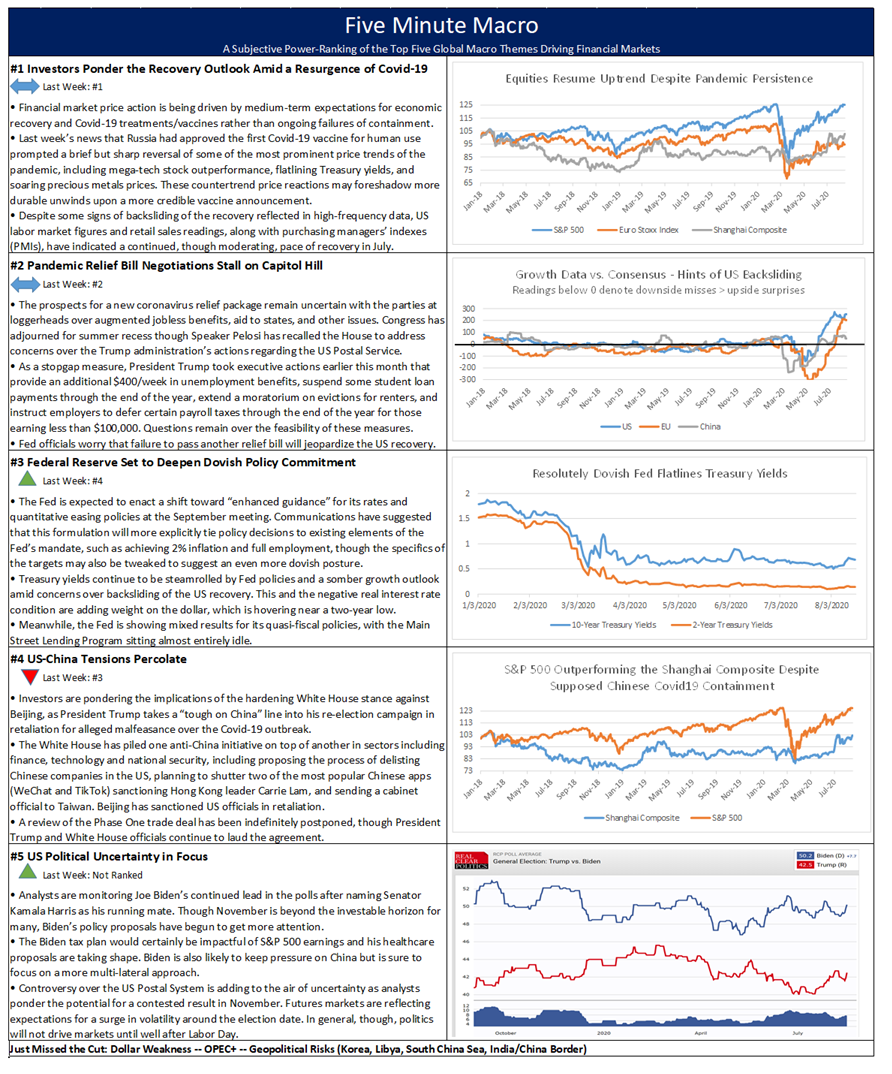

Covid economic recovery and the relief bill negotiations remain front and center on investor’s minds. The Fed’s dovish pivot moves up to third, while US-China tensions moves down a spot. US political uncertainty moves into the last spot.

Covid economic recovery and the relief bill negotiations remain front and center on investor’s minds. The Fed’s dovish pivot moves up to third, while US-China tensions moves down a spot. US political uncertainty moves into the last spot.

Summary and Price Action Rundown

Global risk assets are mostly higher this morning as monetary easing in China overnight set a positive tone to start the week, while investors continue to ponder the prospects for the US pandemic relief package amid deepening rancor in Washington. S&P 500 futures indicate a 0.3% higher open after the index closed flat on Friday, holding its year-to-date gain at 4.4% and hovering just short of February’s all-time high. Equities in the EU are little changed, while Asian stocks were mixed overnight amid outperformance by mainland Chinese markets. The dollar remains subdued near two-year lows while longer-dated Treasury yields are retracing a portion of their recent upside, with the 10-year yield at 0.69%. Brent crude is edging below $45.

US Postal Service Controversy Clouds Pandemic Relief Outlook

Speaker Pelosi called the House back to Washington over the weekend, cutting short summer recess in an effort to address concerns surrounding the Trump administration’s actions impacting the US Postal Service. With President Trump continuing to denigrate mail-in ballots and his administration pursuing changes at the Postal Service that could impede voting by mail, House Democrats are reconvening to push forward efforts to support the USPS and are calling Postmaster General DeJoy to testify on August 24th. White House Chief of Staff Meadows indicated that President Trump would support and sign a bill offering additional $10 billion in funding for the USPS, and though Speaker Pelosi has previously rejected any piecemeal approach to passing elements of the broader pandemic relief bill, analysts note that this could be treated as a standalone given its highly-charged political nature. Analysts broadly note that the controversy over the USPS may remain compartmentalized from the broader negotiations of the pandemic relief package, as the gaps between the two sides persist over state aid and augmented jobless benefits. Meanwhile, financial markets continue to display scant reaction to the DC dramatics, with equity indexes poised to register new record highs this week.

Global Economic Data Remains Mixed with August PMIs in Focus

July’s reading of US retail sales reflected continued but moderating improvement, as investors shift their focus to income August data to gauge the health of the recovery. US retail sales rose 1.2% from a month earlier in July, missing market expectations of 2.1% advance and slowing from an 8.4% month-on-month (m/m) surge in June. In all, it still marked the third straight monthly gain for retail, which plunged 14.7% m/m in April then rebounded to 18.3% m/m in May as the strict lockdowns were eased. July purchases lifted retail sales 2.7% higher than the same month in the previous year, their highest level since the government started tracking the series in 1992. Excluding automobiles, gasoline, building materials and food services, retail sales increased 1.4% m/m in July, topping estimates of a 0.8% gain, after soaring 6.0% in June. Overnight, Japanese GDP data provided another reminder of the pain of the second quarter, with GDP contracting at a 27.8% annualized rate, the steepest drop on record and worse than the 26.9% forecast. The Nikkei underperformed overnight but the yen was stable within its recent trading range versus the dollar. Later this week, analysts will be focused on the first glimpses of global economic activity in August, with preliminary readings of purchasing managers indexes (PMIs) for the US, EU, UK, and Japan, which are expected to show an incrementally accelerating rate of expansion despite the stubborn persistence of the virus.

Additional Themes

People’s Bank of China (PBoC) Injects Liquidity – The Shanghai Composite bounced 2.3% overnight, re-approaching its multi-year high from early July, while the renminbi posted modest gains and local bonds rallied after the PBoC supplied the market with an unexpectedly generous 700 billion renminbi through its medium-term lending facility. This comes after last week’s net injection of funds through open market operations. The PBoC has been notably less aggressive with accommodation than other major global central banks during the ongoing pandemic and key Chinese economic data for July showed a slackening in the pace of recovery, particularly among consumers.

US-China Tensions Continue to Percolate – Reports this morning indicate that the Commerce Department is poised to tighten restrictions on controversial Chinese tech giant Huawei’s access to US technology. This comes after Friday’s news that the planned US-China Phase One trade deal review has been postponed indefinitely, with scheduling problems being cited for the delay. Vice Premier Liu had been set to engage in a video conference with US Trade Representative Lighthizer and Treasury Secretary Mnuchin. President Trump and National Economic Council Director Kudlow both spoke favorably of the Phase One deal last week despite Chinese agricultural goods and energy purchases meaningfully lagging their targets.

Summary and Price Action Rundown

Global risk assets are mixed this morning ahead of key US economic data after China’s growth readings for July broadly met expectations overnight. S&P 500 futures point to a 0.2% lower open after the index wavered yesterday, again falling a few points short of February’s all-time high. Equities in the EU are underperforming as the UK expands its quarantine requirements to more EU countries, while Asian stocks were mixed overnight. The dollar is hovering just above two-year lows while longer-dated Treasury yields are dipping ahead of US retail sales data but still near their highest level since late June, with the 10-year yield at 0.70%. Brent crude prices are edging below $45 per barrel.

Chinese Economic Data Tracks Expected Recovery Trajectory

July economic data out of China overnight reflected continued improvement mostly in-line with forecasts, though retail sales undershot expectations. China’s economy has returned to growth after a deep slump at the start of the year, but some unexpected weakness in domestic consumption weighed on momentum. China’s fixed-asset investment improved to -1.6% year-to-date (ytd) compared to a 3.1% ytd decline registered in June, matching consensus, as the economy continues to re-open and authorities loosen coronavirus-related restriction measures. Private investment, which accounts for 60% of total investment in China, decreased 5.7%, while public investments rose at a faster 3.8%. Investment was driven by acceleration of activity in the property sector, with analysts also expecting the rebound in infrastructure spending to continue over the coming months on the back of government support. Meanwhile, China’s industrial production rose by 4.8% year-on-year (y/y), matching June’s growth rate but below forecasts for a 5.2% expansion. This remained the steepest rise in industrial output in six months, amid ongoing recovery from the pandemic. While investment and industrial production were roughly in line with projections, retail sales registered a disappointing -1.1% y/y, missing expectations of a 0.1% rise but still improving from June’s -1.8% y/y pace. This was the seventh straight month of contraction in retail trade, suggesting a hesitance to return to crowded places like shops, restaurants, and cinemas amid the lingering impact of Covid-19. The decline in retail sales was broad based, with auto sales a key exception, surging 12.3%.

US Retail Sales in Focus

With high-frequency data suggesting a backsliding in US consumption, market participants will be attuned to today’s release of retail sales data for July. Consensus forecasts are for a more modest monthly gain of 2.1% after a 7.5% month-on-month (m/m) snapback in June that brought the gauge into positive year-on-year territory. This would mark the third straight month of upside in retail sales following a record 14.7% slide in April. For context, May’s record 18.2% m/m jump was cited by White House officials as indicative of a brisk economic recovery as states began reopening following lockdowns. The past two months have brought retail sales up to just 0.6% below February’s levels from before the coronavirus pandemic and control group sales, which exclude more volatile autos, gas and building materials, jumped 5% above February’s levels as of last month, underscoring a recovery in consumer spending as lockdown measures eased. Still, rising Covid-19 cases and stalled state re-openings could have deterred shoppers from visiting brick-and-mortar stores, as well as bars and restaurants. The figures may help confirm high-frequency credit card data showing that the consumer recovery has cooled. Other economic data set for release today includes industrial production for July, which is forecast to ease to a 3.0% m/m from 5.4% in June, and University of Michigan consumer sentiment gauge, with estimates for a slight softening to 72.0 from 72.5.

Additional Themes

US Stimulus Talks Remain Deadlocked – Congress has left town for August recess with no deal on the latest pandemic relief package, suggesting that any agreement might slide into September. House Speaker Pelosi stated earlier this week that the sides remain “miles apart” and National Economic Council Director Kudlow reiterated White House concerns that the Democrats’ compromise figure of $2 trillion, which includes a greater measure of state aid than the Republican version, was too high. Meanwhile, President Trump indicated that he would not veto the bill if it contains additional funding for the US Postal Service.

Looking Ahead – Next week features some of the first glimpses of global economic activity in August, with preliminary readings of purchasing managers indexes (PMIs) for the US, EU, UK, and Japan, which are expected to show an incrementally accelerating rate of expansion. Also, analysts will parse the minutes from the Fed’s July meeting, which may include additional insights on their anticipated policy pivot to “enhanced guidance” in September. Also, the US-China Phase One trade deal review is expected to make headlines.

Summary and Price Action Rundown

Global risk assets are mixed this morning after yesterday’s rally took US equity indexes nearly back to record highs, while investors look ahead to key economic data today and tomorrow. S&P 500 futures indicate a slightly lower open after yesterday’s 1.4% rally took the index’s year-to-date gain to 4.6% to come within a few points of February’s all-time high. Equities in the EU and Asia were mixed overnight. The dollar is slipping back toward two-year lows while longer-dated Treasury yields are steady ahead of initial jobless claims data, with the 10-year yield at 0.68%, its highest level since early July. Brent crude prices are fluctuating above $45 per barrel.

US Labor Market Data in Focus

Though last week’s reading of July nonfarm payrolls remained solid, investors are wary of further backsliding in the US recovery and will scrutinize this morning’s weekly jobless claims figures for any signs of weakness. Expectations are for a slight improvement in the figures for the week ending August 8th, with 1.10 million new claims as the consensus forecast. For context, the number of Americans filling for unemployment benefits rose by 1.2 million in the week ended August 1st, the least since the pandemic started and comparing favorably to prior estimates of 1.4 million. It was also the largest weekly drop in jobless benefits applications in almost two months. This follows a solid reading for last week’s highly-anticipated July nonfarm payrolls figures, which showed the US economy added 1.76 million jobs in July, down from a record 4.8 million in June but well above market expectations of 1.6 million. This put nonfarm employment 12.9 million below the pre-pandemic level and pushed the unemployment rate down to 10.2% from 11.1%, which bettered consensus expectations of 10.5%. The number of unemployed persons fell by 1.4 million to 16.3 million, putting the labor force participation rate 61.4%, down slightly from 61.5% in June. Tomorrow also features potentially market-moving US economic data, with July retail sales in the spotlight, along with industrial production for last month and consumer sentiment data for August.

Fed Communications Retain a Decidedly Dovish Tone

With analysts anticipating a policy shift by the Fed perhaps as early as the September meeting, commentary from FOMC officials remains highly focused on the downside risks. Boston Fed President Rosengren and Dallas Fed President Kaplan spoke separately yesterday, focusing on the need for redoubled efforts at pandemic containment alongside additional fiscal stimulus to prevent the economic recovery from backsliding. Rosengren said that “despite the sizeable interventions by monetary and fiscal policymakers, high-frequency economic data indicate that the recovery may be losing steam,” causing him to worry that an increasing number of temporary layoffs may turn into permanent job losses. Kaplan sounded a similar note, saying, “the rebound continues but, with the resurgence of the virus in a number of locations in the United States, that has muted the rebound…. A number of countries around the world have gotten the virus transmission rates to relatively low levels and are recovering at a very rapid rate.” For context, analysts are expecting the FOMC to pivot to a new policy of “enhanced guidance” at their September meeting, which would more formally link interest rate and asset purchase policies to their 2% inflation and full employment targets.

Additional Themes

Pandemic Relief Talks Remain Deadlocked – House Speaker Pelosi declared yesterday that the two sides remained “miles apart” after Secretary Mnuchin brought an offer of a bill that would be just above $1 trillion, representing little give from the administration’s previous position. Mnuchin indicated that another follow-on bill could be considered if the Democrats would first agree to this less-ambitious version. For context, the White House issued stopgap executive orders to provide some degree of stimulus in lieu of a Congressional spending package, though questions remain over the efficacy, enforceability, and timeframe of these measures. The four orders signed provide an additional $400/week in unemployment benefits, suspend some student loan payments through the end of the year, extend a moratorium on evictions for renters, and instruct employers to defer certain payroll taxes through the end of the year for Americans earning less than $100,000.

Corporate Concern Over WeChat – Analysts are citing a report this morning indicating that management of Apple and more than a dozen other key US corporations raised concerns on a call with the White House about the impact on their business from the impending ban on WeChat. For context, President Trump announced last week that Chinese-owned social media apps WeChat and TikTok would be banned from the US as of mid-September. Chinese officials are set to raise this issue in the Phase One trade review with their US counterparts scheduled for this coming week.

Summary and Price Action Rundown

Global risk assets are rebounding this morning after yesterday’s selloff, while Treasury yields are continuing to rise ahead of US inflation data. S&P 500 futures indicate a 0.8% higher open after yesterday’s 0.8% decline pared the year-to-date gain to 3.2%, with the index hovering around 1% below February’s all-time high. Equities in the EU and Asia were muted and mixed overnight. The dollar is fluctuating near two-year lows while longer-dated Treasury yields are extending their upside, with the 10-year yield at 0.67%, its highest level since early July. Brent crude prices are back above $45 per barrel.

US Inflation Figures in Focus

After yesterday’s release of producer price inflation showed faster-than-anticipated increases in price pressures, the focus today will be on the consumer price gauge (CPI). With longer-dated Treasury yields vaulting higher yesterday and continuing to move upwards this morning, traders will be particularly attuned to this morning’s US CPI reading for July, with an upside surprise likely to fuel a further rise in Treasury yields. US CPI increased to 0.6% in June from May’s four-and-a-half-year low of 0.1% and is expected to edge up to 0.7% for July. June’s pace of price increases was the fastest in three months as businesses reopened after the coronavirus lockdown, led by food and food at home prices, as well as energy costs and medical care services. On a monthly basis, prices went up 0.6% in June, the most since August of 2012, slightly beating market consensus of a 0.5% gain. The annual US core consumer price inflation rate, which excludes volatile items such as food and energy, stood at 1.2% year-on-year in June, unchanged from the previous month’s nine-year low and slightly above market expectations of 1.1%. For context, the Fed targets 2% inflation and may pivot to “enhanced guidance” at the September meeting, which would more formally link interest rate and asset purchase policies to this benchmark. However, the Fed favors an alternate inflation metric, core PCE, over CPI. Yesterday, US producer prices (PPI) rose 0.6% in July from a month earlier, reversing the 0.2% decline in June and beating forecasts of only a 0.3% gain. Last month’s data marked the largest increase in producer prices since October 2018, mainly driven by rising energy costs following the easing of coronavirus-induced restrictions.

UK Data Reflects Deep Recession

UK GDP figures for the second quarter (Q2) showed a worse slump than any other major European economy, shrinking by a fifth and falling into its deepest recession on record. A preliminary estimate indicated that UK gross domestic product shrank by 20.4% on quarter (q/q) and 21.7% from a year prior in Q2, equivalent to an annualized rate of 59.8%, the most since comparable records began in 1955, which was roughly in line with expectations of a 20.5% quarterly contraction. A recovery from the depths of the lockdown gained momentum in June, with output growing 8.7% from the prior month, faster than most economists had expected, although broadly in line with the Bank of England’s latest predictions. This means GDP has grown 11.3% since its April low, but remains 17.2% beneath its level in February, before the coronavirus crisis hit. Analysts said the UK’s underperformance was partly due to the length of its lockdown, and partly because the consumer-facing services sector that was hardest hit by social distancing has a bigger weight in GDP, accounting for 80% of the economy. Private consumption accounted for more than 70% of the decline in the GDP, down by 23.1%. There was also notable retrenchment in gross fixed capital formation (-25.5%) and government consumption (-14.0%). The services sector fell 19.9% q/q, accounting for three-quarters of the fall in GDP.

Additional Themes

Kodak Mum on Loan – After the market closed yesterday, Eastman Kodak released its second quarter earnings report posting a net loss of $5 million and $213 million in revenue, down 31% year-over-year. While investors were interested in the financial state of the company and its resilience to the pandemic, the main focus was on updates regarding the proposed $765 million Defense Production Act loan from the International Development Finance Corporation (IDFC). Shares experienced meteoric gains in recent weeks upon news of a potential government loan to fund the operational restructuring towards establishing Kodak as a major domestic supplier of pharmaceutical ingredients. However, shares toppled 28% over the past week amid allegations of insider trading by Kodak executives who had prior knowledge of the potential deal. On Monday, the White House responded that Kodak will not receive the loan unless the company is cleared of wrongdoing. During the earnings call yesterday evening Kodak stated it will not “discuss the potential loan or the related matters” as the company is currently under internal review. Kodak also chose to not hold a Q&A session post-conference. While investigators are currently conducting an internal review of Kodak’s executives’ actions, public disclosures filed with Congress reveal Kodak spent $870,000 lobbying Congress and federal agencies during the second quarter. The last time the company spent on lobbying was $5,000 in Q1 2019.

US-China Trade in Focus – Reports this morning indicate that China is intent on bringing the impending US bans on TikTok and WeChat into the Phase One trade deal review talks schedule for the middle of this month. China’s agricultural purchase commitments are another key issue.

Summary and Price Action Rundown

Global risk assets are advancing this morning after Russia’s announcement that a domestically-produced vaccine has been approved for use, while President Trump mulls additional options for stimulus amid deadlocked talks with Congress over the pandemic relief bill. point to a 0.5% higher open after yesterday’s gains extended the index’s year-to-date upside to 4.0%, registering a new high for the pandemic and coming within 1% of February’s all-time high. Equities in the EU are jumping on the vaccine news and encouraging economic data, while Asian stocks were mostly higher overnight. The dollar is turning back toward nearly two-year lows while longer-dated Treasury yields are finding support on vaccine hopes, with the 10-year yield at 0.61%. Brent crude prices are rising above $45 per barrel.

Optimism Over Russian Vaccine News

Russia’s announcement that a Covid-19 vaccine has been approved is providing further impetus for the ongoing rally in global equity markets. Earlier this morning, global risk asset prices lurched higher following news that Russia’s Health Ministry has issued the world’s first approval for a Covid-19 vaccine, which has been developed by the Gamaleya Institute. President Putin declared that it provides lasting immunity, with the Health Ministry estimating a two-year period of effectiveness, and that his daughters have each received a dose. Reports have registered a degree of skepticism from the global medical community, with concerns that the standard Phase 3 trial period had been radically shortened or skipped entirely in an effort to rush the vaccine to market. With a profusion of potential vaccines in various stages of development, investors have been poised for a series of vaccine announcements beginning roughly around now, though there continues to be deep uncertainty over their effectiveness as well as the ability to produce and distribute them widely enough to achieve herd immunity in a timely fashion.

White House Eyes Tax Cuts Amid Congressional Deadlock on Stimulus

After President Trump moved to circumvent Congress over the weekend with stopgap pandemic relief measures through executive order, his remarks last evening revealed a pivot to prospective tax cuts. At a press conference yesterday, President Trump indicated that he is revisiting the idea of reducing capital gains tax rate, which tops out at 20%, and will seek to deliver a middle-class tax cut, noting that details would follow shortly. However, analysts point out that his ability to enact these measures without Congressional assent is limited, though an executive order could in theory be used to require capital gains to be indexed to inflation, thereby effectively reducing the rate paid. Such an approach has been considered previously and is deemed likely to face legal challenges. This comes as questions mount over the efficacy of President Trump’s executive orders issued in lieu of a pandemic relief deal. Amid mixed messages from the White House regarding the payroll tax holiday, businesses must assume that they will to have to pay back the deferred amounts later this year, while more states are pushing back regarding their obligation under the President’s unemployment relief to pay a quarter of the $400 additional benefit. Meanwhile, House Democrats and administration officials remain at loggerheads over key negotiating points, particularly the amount of unemployment benefit support and aid to states and municipalities.

Additional Themes

Australian Business Confidence Slips – The National Australia Bank’s (NAB) index of business confidence plunged to -14 in July from a downwardly revised 0 in the prior month, amid uncertainties surrounding the Covid-19 resurgence that led to renewed restrictions in Victoria. Confidence fell across all industries, led by a decline in mining. The survey was conducted prior to the stage 4 lockdown in Melbourne but confidence had already deteriorated for fear of the spread of the coronavirus. The NAB Group Chief Economist said, “while the improvement in conditions is very welcome, capacity utilization and forward orders point to ongoing weakness overall. Therefore, with confidence still fragile there is some risk that conditions lose some of their recent gains in coming months.”

EU Economic Outlook Brightens – The closely-followed ZEW economic expectations survey showed improvement in August for both Germany and the EU as a whole. The German reading jumped to 71.5 from July’s reading of 59.6, handily topping consensus estimates of 55.8, while the regional gauge advanced to 64.0 from 59.6. For context, recent upside surprises in EU economic data have contributed to gains for euro, sending the single currency to its highest level versus the dollar since spring of 2018.

US Small Business Confidence Dips – The NFIB small business optimism index undershot expectations in July, declining to 98.8 from June’s multi-month high of 100.6 versus estimates of only a slight tip to 100.5. The NFBI chief economist noted the difficulties that small businesses faced last month in attempting to reopen amid a widespread Covid-19 resurgence.

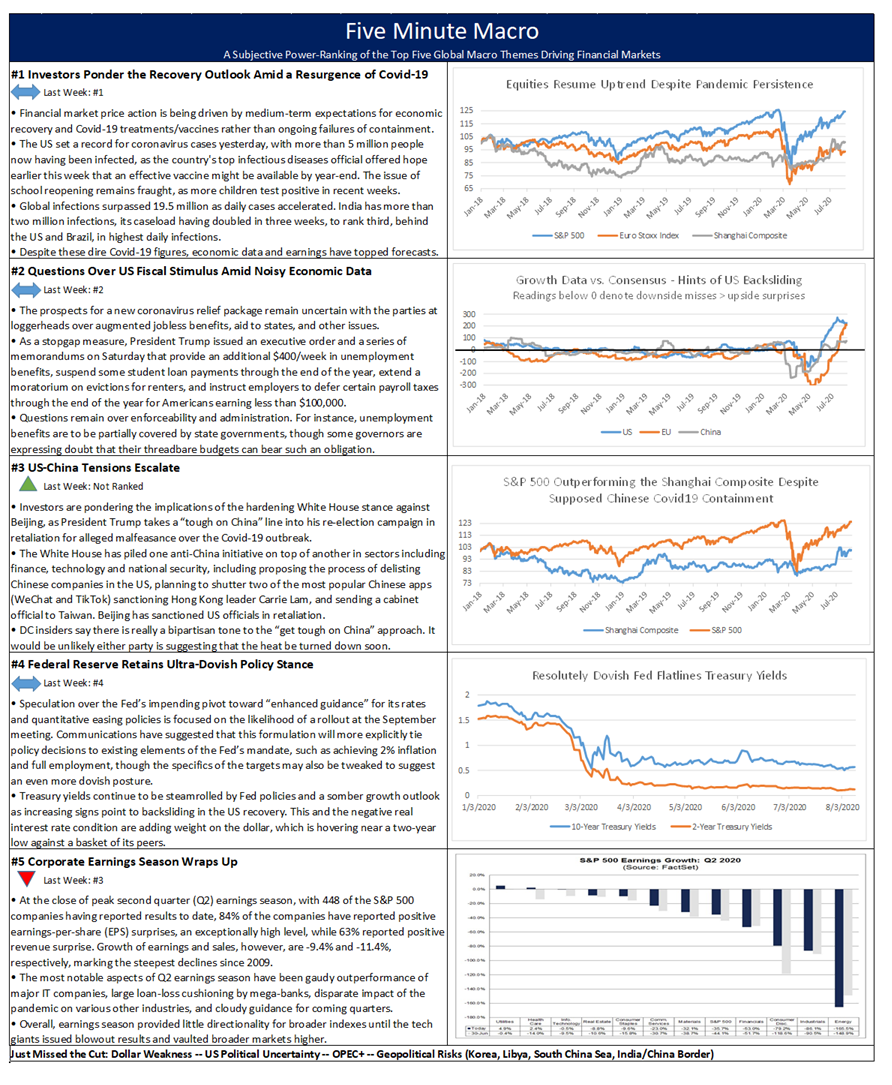

Recovery and the Pandemic remain first, while fiscal stimulus deadlock stays second. US/China tensions are brewing this week but the Fed remains ultra-dovish. Finally, corporate earnings wrap up this week.

Summary and Price Action Rundown

Global risk assets were mostly higher overnight as President Trump attempts to circumvent Congress to deliver pandemic relief through executive action, while US-China tensions continue to percolate but stop short of significant escalation. S&P 500 futures indicate a slightly higher open after last week’s gains extended the index’s year-to-date gain to 3.7%, registering a new high for the pandemic and coming within nearly 1% of February’s all-time high. Equities in the EU and Asia were mostly higher overnight. The dollar is continuing to claw higher from nearly two-year lows though longer-dated Treasury yields are settling back toward recent lows, with the 10-year yield at 0.55%. Brent crude prices are re-approaching $45.

White House Resorts to Executive Action Stimulus Stopgaps

After the administration failed to reach an agreement last week with Congressional Democrats over the magnitude and priorities of the next round of US pandemic relief spending, President Trump took executive actions over the weekend that have raised questions of enforceability and administration. President Trump issued an executive order and a series of memorandums targeted at coronavirus stimulus on Saturday, moves which some analysts characterize as bypassing Congressional authority over the purse, as stimulus talks remained at an impasse following another contentious week of negotiations. There is no apparent schedule for talks to restart today. The four orders signed provide an additional $400/week in unemployment benefits, suspend some student loan payments through the end of the year, extend a moratorium on evictions for renters, and instruct employers to defer certain payroll taxes through the end of the year for Americans earning less than $100,000. Unemployment benefits are to be mostly covered by the federal government ($300/week) with state governments providing the remaining $100/week, though some governors are expressing doubt that their threadbare budgets can bear such an obligation. The duration of these payments is also unclear, as is the timeline for disbursement of funds to eligible recipients. Meanwhile, the Trump administration has sent mixed messages on the details of the payroll tax holiday, raising confusion over its application. The breakdown in negotiations leaves several other issues, from stimulus checks to PPP funding, on hold until an agreement can be reached.

US-China Tensions Remain Elevated

In retaliation for the latest US moves to counter China, including sanctions on eleven high-ranking officials involved in oppression in Hong Kong and the impending bans on Chinese-owned apps TikTok and WeChat, Beijing announced that it would sanction eleven US officials. Senators Rubio and Cruz are two high-profile names on the list, but with China matching the US figure of eleven targeted individuals and no Trump administration officials on the list, there is a sense of proportionality and de-escalatory intent suggested in this move. For context, last week featured high-profile moves by the Trump administration targeting China and Chinese companies with alleged deep government ties. Friday morning, the US announced that it was imposing sanctions on eleven Chinese officials including Hong Kong’s Chief Executive Carrie Lam over their role in “implementing Beijing’s policies of suppression of freedom and democratic processes” according to the Treasury Department. This move followed recent executive orders from the administration that will impose a ban on Chinese-based apps TikTok and WeChat in the US amid privacy and national security concerns. Relatedly, the scramble by US companies to arrange potential bids for TikTok’s US business continues to heat up, with Twitter now in the mix along with Microsoft and other companies. Equities in Hong Kong underperformed overnight, though mainland Chinese equities rallied and both the onshore and offshore renminbi remained stable against the dollar near their strongest levels since March.

Additional Themes

Kodak Deal on Hold – The $765 million 25-year loan from the International Development Finance Corporation to expedite domestic production of drugs for several medical conditions, authorized by the Defense Production Act, has been delayed amid allegations that Eastman Kodak board members engaged in improper stock purchases ahead of the disclosure. Upon the announcement of the loan late last month, shares of the former photo giant soared over 300% and continued to rise over the ensuing days, gaining roughly 1000% over the course of that week.

Pivotal Global Economic Data This Week – This week, US retail sales figures for July offer the greatest potential for moving markets, as analysts will be attuned for signs that the resurgence of Covid-19 last month dented consumer sentiment. Meanwhile, initial jobless claims and consumer price inflation will also be in focus. Overseas data includes key Chinese growth readings for July, as well as second quarter EU and UK GDP.

Summary and Price Action Rundown

Global risk assets were mostly lower overnight amid rising US-China tensions and uncertainty over US fiscal stimulus negotiations, while investors await this morning’s key US labor market data. S&P 500 futures point to a 0.4% lower open after the index rose another 0.6% yesterday to extend its year-to-date gain to 3.7%, registering a new high for the pandemic and coming within nearly 1% of February’s all-time high. Equities in the EU and Asia were mostly lower overnight. Ahead of the pivotal US jobs number, the dollar is climbing above almost two-year lows while longer-dated Treasury yields are flat around their lowest levels since early March, with the 10-year yield at 0.53%. Brent crude prices are dipping below $45 per barrel.

US Labor Market in the Spotlight

After some mixed employment data earlier this week raised questions over the durability of the US jobs market recovery, investors are awaiting July nonfarm payroll figures. The Labor Department’s highly-anticipated July employment numbers are due later this morning, with consensus estimates for 1.48 million new jobs after June’s record 4.80 million. Following a spurt of hiring over recent months amid the selective reopening of the economy, economists are pondering a leveling-off in improvement. Yesterday’s new jobless claims data for the week ending August 1st showed that another 1.2 million Americans filed for unemployment benefits, the least since the pandemic started, 200k less than last week and comparing favorably to consensus expectations of 1.4 million. It was also the largest weekly drop in jobless benefits applications in almost two months, but still the 20th consecutive week of over a million claimants. Earlier this week, data showed a steep deceleration in private payrolls in July as payroll provider ADP reported that private businesses in the US hired just 167,000 workers last month, far short of market expectations of a 1.5 million rise after a revised 4.3 million increase in June. With ADP and continuing claims sending somewhat disparate signals, analysts will be particularly attuned to this morning’s nonfarm payrolls report.

US-China Tensions Ratchet Higher

In the latest move to counter China and its international companies with alleged ties to the Chinese Communist Party, President Trump banned apps TikTok and WeChat, effective in 45 days. President Trump invoked the 1977 International Emergency Economic Powers Act to justify the bans on US companies dealing with Chinese parent companies ByteDance and with Tencent specifically in connection with WeChat. The law provides a broad mechanism for the US government to impose restrictions on companies deemed to pose a threat. The TikTok order formalizes President Trump’s announcement earlier this week that app would be blocked in the US unless a US buyer completes a deal for the business within 45 days. Once the order takes effect, at the end of that period, any transactions between TikTok’s parent company, ByteDance, and US citizens will be outlawed for national security reasons. For the more than 100 million Americans who have downloaded TikTok, experts say the app may no longer be sent software updates, rendering TikTok inoperable over time. President Trump yesterday renewed calls for Microsoft to acquire the app and suggested that it should try to buy TikTok’s entire global operations. Secretary of State Pompeo signaled that the crackdown on TikTok was part of a broader campaign against Chinese tech companies with access to the data of US citizens. On Thursday, in a display of bipartisan solidarity on this issue, the Senate unanimously passed a bill to ban TikTok on government-issued devices. Trump also signed an executive order to restrict US business with China-based Tencent Holdings but narrowly in regard to its WeChat app. More than a billion people in China use WeChat, an all-in-one app used for messaging, social media and making mobile payments. Additionally, a White House working group also put forward a plan that Chinese companies with shares traded on US stock exchanges would be forced to de-list unless they comply with specific audit requirements by 2022. Chinese firms that are planning an initial public offering in the US would have to comply before they can be listed. The administration’s plan would require rule-making by the SEC, which ultimately oversees the audits of companies whose shares are traded in the US.

Additional Themes

US Stimulus Talks on the Brink – With today seen as an unofficial deadline for a deal, the atmosphere around the negotiations has turned more contentious. Speaker Pelosi and Senate Minority Leader Schumer expressed disappointment with yesterday’s talks, saying that the two sides are far apart on key issues. This dour assessment was echoed by Treasury Secretary Mnuchin and WH Chief of Staff Meadows. President Trump continues to assert that he will enact economic relief measures through various executive orders in lieu of a deal.

Earnings Feature Pandemic Impact – As earnings season winds down this week, analysts are focused on some notable reports from companies impacted by the pandemic. Shares of Uber are down 3.5% in pre-market trading after soaring Uber Eats deliveries failed to offset the steep decline in customer rides. With 441 of S&P 500 companies having reported, 84.3% of results have featured a positive earnings-per-share (EPS) surprise and 63.9% have topped revenue estimates. However, growth of sales and earnings are down 11.2% and 9.3%, respectively, thus far year-on-year.

Summary and Price Action Rundown

Global risk assets are mostly lower ahead of this morning’s key US labor market data, while investors monitor halting progress toward a US pandemic stimulus bill. S&P 500 futures indicate a 0.2% lower open after the index rose 0.6% yesterday to extend its year-to-date gain to 3.0%, registering a new high for the pandemic and coming within 2% of February’s all-time high. Equities in the EU and Asia were mixed overnight. The dollar is hovering near two-year lows while longer-dated Treasury yields are sliding back toward their lowest levels since early March, with the 10-year yield at 0.52%. Brent crude prices are holding above $45 per barrel.

Uncertainty Over US Labor Market Recovery

Following yesterday’s disappointing US jobs figures for July, analysts are awaiting this morning’s release of weekly unemployment claims data and looking ahead to tomorrow’s consequential nonfarm payroll figures. According to payroll provider ADP, private businesses in the US hired just 167,000 workers in July, far short of market expectations of a 1.5 million rise after a revised 4.3 million increase in June. The labor market continued to recover from April’s record slump in employment, but a resurgence in Covid-19 infections has forced several states to scale back or pause the reopening of their economies, sending some workers back to unemployment. Businesses with between 50 and 499 employees reported an outright decline of 25,000. Big business brought back 129,000 jobs while firms with fewer than 50 workers added just 63,000. All but 1,000 of the jobs came from the services sector, as professional and business services led with 58,000 while the battered hospitality sector saw an addition of 38,000. Analysts are now awaiting today’s weekly jobless claims data, with expectations for a relatively stable 1.40 million new filings for the week ending August 1st versus 1.43 million the prior week. This will set the stage for the Labor Department’s highly-anticipated July nonfarm payrolls figures, which will be released tomorrow morning. Consensus estimates are for 1.50 million new jobs after June’s record 4.80 million.

Bank of England Holds Policy Steady

The UK central bank deferred its decision on additional easing into the fall as it monitors the ongoing economic effects of the pandemic and eyes the risk of hard Brexit at year-end. The Bank of England (BoE) voted unanimously today to maintain the key bank rate at a record low of 0.1%, in line with analysts’ expectations as this summer meeting was generally seen as a placeholder ahead of the BoE’s likely more consequential decisions at either the September or November meetings. The Committee also voted unanimously for the BoE to continue with its existing programs of UK government bond and sterling non-financial investment-grade corporate bond purchases, maintaining the target for the total stock of these purchases at £745 billion. The Committee expressed the intention not to tighten monetary policy until there is clear evidence that significant progress is being made in eliminating spare capacity and achieving the 2% inflation target sustainably and Governor Bailey downplayed the prospect of negative interest rate policy (NIRP). Some analysts had expected the BoE to take a more proactive approach at this meeting, perhaps increasing the magnitude of asset purchases, with that option now being deferred to September or November, while futures markets are now reflecting diminished odds of NIRP. As market participants recalibrate to account for the slightly less dovish than anticipated BoE policy stance, the pound is getting a boost this morning, rising 0.5% versus the dollar to approach its 2020 high from January. Still, further easing is anticipated amid ongoing headwinds from the pandemic and the threat of a no-deal Brexit at year-end.

Additional Themes

Clock Ticks Down on US Stimulus – With tomorrow seen as an unofficial deadline for a deal before possible Congressional recess, mixed reports of progress towards a consensus continue. Speaker Pelosi, Senate Minority Leader Schumer, Treasury Secretary Mnuchin and WH Chief of Staff met again yesterday afternoon, with the Trump administration offering to extend federal unemployment insurance at $400 per week and the moratorium on evictions from federally backed housing into December, alongside $200 billion in aid for states and municipalities. Though progress was cited, no agreement was forthcoming.

Earnings Feature Pandemic Impact – As earnings season winds down this week, analysts are focused on some notable reports from companies impacted by the pandemic. Disney traded 8.9% higher yesterday after announcing a solid performance driven by impressive growth in its Disney+ streaming service that now totals 60.5 million subscribers. Meanwhile, analysts are bracing for ugly numbers from Uber after today’s closing bell. With 415 of S&P 500 companies having reported, 84.2% of results have featured a positive earnings-per-share (EPS) surprise and 64.2% have topped revenue estimates. However, growth of sales and earnings are down 11.5% and 10.3%, respectively, thus far year-on-year.