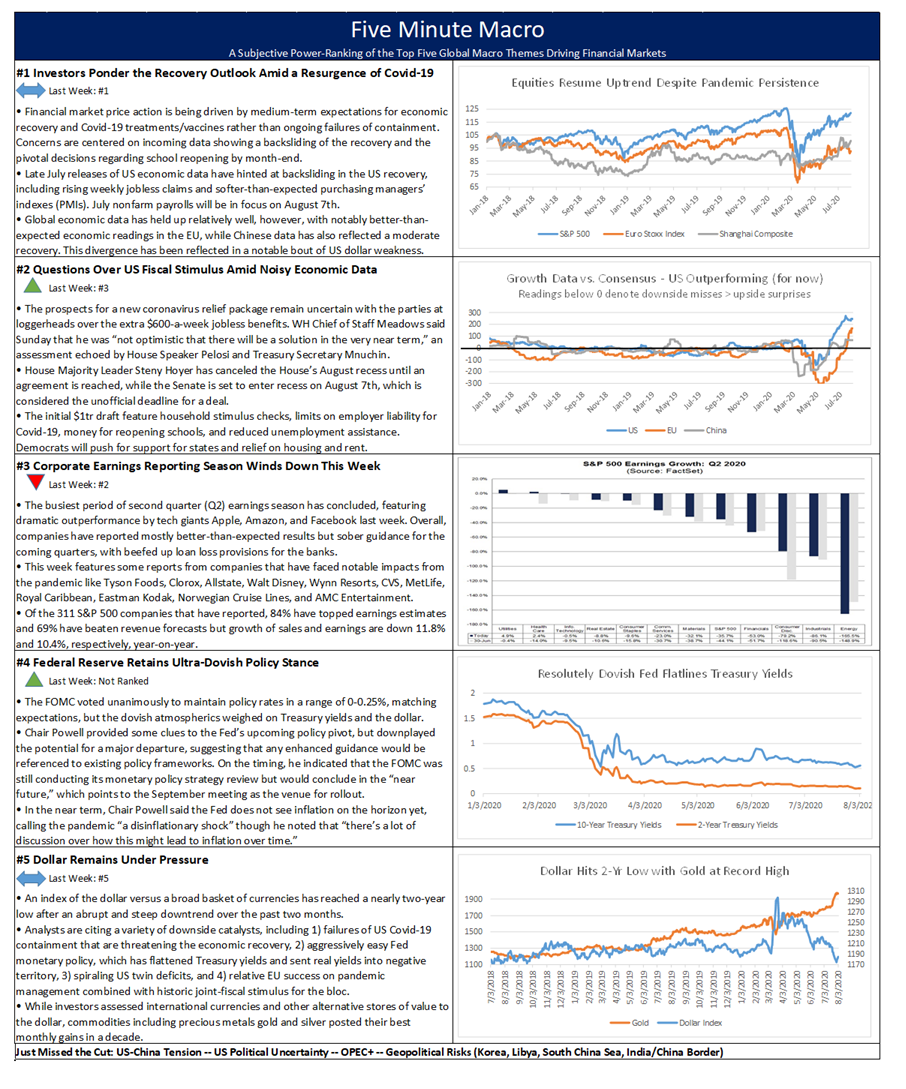

Pandemic recovery remains front and center but worries about CARES/HEROES 4 moves up to second. Corporate earnings drops to third while a dovish FOMC stance enters at 4 with dollar weakness remaining in the fifth spot.

Pandemic recovery remains front and center but worries about CARES/HEROES 4 moves up to second. Corporate earnings drops to third while a dovish FOMC stance enters at 4 with dollar weakness remaining in the fifth spot.

Summary and Price Action Rundown

Global risk assets were mostly higher overnight with some solid economic data supporting sentiment despite ongoing US-China tensions, while last week’s strong earnings from IT giants look set to extend US equity gains despite uncertainty over the latest US pandemic stimulus bill. S&P 500 futures point to a 0.5% higher open after the index rose 0.8% on Friday to put gains for the week at 1.7%, moving further into positive territory for the year but staying just shy of mid-July’s peak for the pandemic. The tech-heavy Nasdaq is poised to extend its outperformance. Equities in the EU and Asia posted gains overnight. The dollar downtrend is pausing again this morning and longer-dated Treasury yields are rising from their lowest levels since early March, with the 10-year yield at 0.55%. Brent crude prices are turning lower toward $43 per barrel as traders remain wary of rising OPEC output amid ongoing demand weakness.

Agreement on US Pandemic Relief Bill Remains Elusive

Congressional leaders and Trump administration officials continued negotiations over the weekend, but the sides remain stalemated over the issues of enhanced unemployment benefits. With the additional $600 per week in jobless benefits mandated by the CARES Act officially expiring on Friday, apparent urgency on both sides of the aisle to find a deal has not yet borne fruit. The need for extending some degree of augmentation is widely acknowledged but Treasury Secretary Mnuchin over the weekend continued to reiterate the position of Congressional Republicans and the White House that $600 is too generous and disincentives beneficiaries to return to work, while Speaker Pelosi indicated on Sunday that Democrats are united in pushing to retain that amount. Late last week, White House officials offered an extension of the $600 benefits for one week, and again suggested separating this issue from the larger stimulus package, a proposal that Democrats rejected, in keeping with their ongoing resistance to a piecemeal approach to the relief bill. House Speaker Pelosi, Senate Minority Leader Schumer, Secretary Mnuchin, and White House Chief of Staff Meadows are reportedly set to meet again today. House Majority Leader Steny Hoyer has canceled the House’s August recess until an agreement is reached, while the Senate is set to enter recess on August 7th. Meanwhile, Senator Romney and a group of other Republican Senators have proposed a 3-month extension to the expanded benefits that would allow states the option of a gradually decreasing flat rate ($500 in August, $400 in September, etc.) or replace 80% of a worker’s usual wages. States would also be allotted $2 billion to update unemployment insurance systems to facilitate the targeted wage replacement.

US-China Tensions Flare Over Social Media

After President Trump indicated that he would move to ban a Chinese-owned social media platform from the US, investors are pondering the ramifications of the decision. In the latest escalation of friction between Washington and Beijing, President Trump ordered ByteDance, the Chinese owners of popular but controversial video-sharing app TikTok, to exit its US operations on Friday. Over the weekend, amid expressions of interest by Microsoft to purchase TikTok’s business lines in the US, Canada, Australia, and New Zealand, the White House set an unofficial deadline until September 15th for the deal to be finalized. For context, TikTok has been criticized by US officials and a number of its US competitors for censorship, alongside allegations of ties to the Chinese military. Its 2017 purchase of another app that helped launch its popularity in the US is still under review by the Committee on Foreign Investment in the United States (CFIUS), which is Chaired by Treasury Secretary Mnuchin. TikTok has 165 million users in the US and 2 billion worldwide. Regarding potential retaliation, Beijing has limited options for a directly proportionate response given that it already bans Facebook, Twitter, and Google. Over the weekend, Secretary of State Pompeo indicated that other Chinese-owned software platforms would also be facing restrictions.

Additional Themes

Earnings Season Rolls On – The busiest and most consequential period of second quarter (Q2) earnings season has concluded, featuring dramatic outperformance by US tech giants Apple, Amazon, and Facebook last week. However, this week still features some meaningful reports, including companies that have faced notable impacts from the pandemic. Tyson Foods, Clorox, Allstate, Prudential, Walt Disney, Wynn Resorts, CVS, MetLife, Etsy, Royal Caribbean, Eastman Kodak, AMC Entertainment, and Norwegian Cruise Lines are among the headliners this week. With 313 of S&P 500 companies having reported, 85.0% of results have featured a positive earnings-per-share (EPS) surprise and 66.4% have topped revenue estimates. However, growth of sales and earnings are down 11.8% and 10.4%, respectively, thus far year-on-year.

July PMIs Reflect Recovery – China’s privately-compiled manufacturing purchasing managers’ index (PMI) for July registered 52.8 versus a forecast of 51.1 and the prior month’s 51.2 reading. Meanwhile, the final readings of EU and Japanese manufacturing PMIs were revised higher from their preliminary estimates released last month, though the latter remained in contractionary territory. For context, PMI readings above 50 denote expansion of the sector. US PMIs for July are due later this morning.

Summary and Price Action Rundown

Global risk assets were mostly higher overnight after strong earnings reports from US tech giants, though investors note mixed economic data and uncertainty over the latest US pandemic stimulus bill. S&P 500 futures indicate a 0.3% higher open as this week’s meandering price action continues, with the index holding in slightly positive territory for the year but remaining below last Wednesday’s peak for the pandemic. Equities in the EU and Asia mostly gained overnight. Ongoing dollar weakness is pausing this morning, but longer-dated Treasury yields are still sinking, with the 10-year yield at 0.54%, its lowest level since early March. Brent crude prices continue to hover above $43 per barrel as demand concerns remain a headwind.

Tech Stocks Lead Higher After Strong Earnings

Amid the busiest stretch of second quarter (Q2) earnings season, tech outperformance keeps rolling following yesterday afternoon’s strong results from IT giants. After the market close, Apple, Amazon, Google, and Facebook all reported impressive earnings and revenues, beating estimates across the board and their shares are mostly higher in pre-market trading. Amazon topped expectation for massive revenue growth from e-commerce, while Apple outpaced revenue and iPhone sales estimates. Analysts were focused on how a reduction in ad spending affected Facebook and Google in Q2 and the initial stock reactions are positive for Facebook, though Google is lagging this morning. While the S&P 500 index has been struggling to remain within positive year-to-date territory, the outperformance of tech stocks has remained near recent extremes despite some modestly corrective activity in recent weeks. Shares of Amazon, Apple, Facebook, Netflix, Google, and Microsoft are up 65.2%, 31.0%, 14.3%, 50.1%, 14.5%, and 29.3%, respectively, year-to-date. By contrast, indexes of US financials, industrials, and materials stocks are -23.1%, -10.3%, and -4.2% on the year. Thus far, aside from spurring more lopsided gains for IT giants, Q2 earnings has provided little overall direction to the broader indexes despite a high degree of upside surprises over sales and profit forecasts. With 305 of S&P 500 companies having reported, 84.4% of results have featured a positive earnings-per-share (EPS) surprise and 66.9% have topped revenue estimates. However, aggregate growth of sales and earnings are down 9.7% and 11.2%, respectively, thus far year-on-year.

Global Economic Data Reflects Uneven Recovery

After yesterday’s release of US Q2 GDP, which showed a historically steep contraction, and further deterioration in labor market indicators, economic data from around the world showed a mixed picture overnight. Chinese manufacturing surprised with yet another month of growth in July over expectations of a minor softening. The manufacturing PMI in China unexpectedly rose to 51.1 from 50.9 in the previous month, compared with market estimates of 50.7. A total of 17 out of the 21 industrial sectors recorded PMIs above the 50 threshold for expansion, compared with only 14 sectors recording growth in June. This was the fifth straight month of increase in factory activity and the strongest since March, as the mainland economy continues to recover after the government lifted strict lockdowns and ramped up investment. Meanwhile non-manufacturing PMI edged down to 54.2 from 54.4, the fifth consecutive month of growth in the service sector as sentiment strengthened markedly. Also in Asia, Japan’s consumer confidence index rose slightly in July, improving for a third straight month to its best level since March, but a recent surge in coronavirus cases suggest a murky outlook for the economy. In the EU, GDP contracted sharply in Q2, underperforming the US with a decline of 12.1% over the prior quarter and down 15.0% year-on-year (y/y). Regional inflation for July remained soft at 0.4% y/y but above forecasts of 0.2%. The euro is slightly lower this morning but remains near its strongest level versus the dollar in over two years. Later this morning, June US personal spending and income data, along with the Fed’s preferred inflation metric, are due.

Additional Themes

Unemployment Benefits in Focus as Congress Debates Relief Bill – Negotiations continue to drag on in Washington over the Republican HEALS Act as augmented unemployment benefits are set to expire today. The wrangling is centered around the amount of these unemployment benefits, as well as over aid for states and localities to bolster their budgets.

Looking Ahead – Next week, the calendar features potentially market-moving US economic data, with July nonfarm payrolls in the spotlight amid consensus estimates of 1.6 million jobs added after June’s 4.8 million, though estimates vary widely and even range into negative territory. Also on the calendar are US purchasing managers’ index readings for July, which will be scrutinized for signs of backsliding amid the resurgence of Covid-19 in various states around the country. The Bank of England and Reserve Bank of Australia also meet next week. The continuation of Q2 earnings season will bring reports from Tyson Foods, Clorox, Allstate, Prudential, Walt Disney, Wynn Resorts, CVS, MetLife, Etsy, Royal Caribbean, Eastman Kodak, AMC Entertainment, and Norwegian Cruise Lines.

Summary and Price Action Rundown

Global risk assets turned lower overnight ahead of the busiest day of corporate earnings season, which will feature reports from IT giants, while investors mull yesterday’s Federal Reserve decision, await key economic data, and monitor wrangling on Capitol Hill over the latest pandemic stimulus bill. S&P 500 futures point to a 1.3% lower open after yesterday’s 1.2% rally took the index back into slightly positive territory for the year as it continues to fluctuate below last Wednesday’s peak for the pandemic. Equities in the EU and Asia also retreated overnight. The ongoing dollar downtrend is pausing today, while longer-dated Treasury yields are sinking, with the 10-year yield at 0.55%, its lowest level since early March. Brent crude prices are sliding below $43 per barrel amid demand concerns.

Federal Reserve Remains Focused on Downside Risks

With policy settings remaining unchanged as expected, investors focused on the resolutely dovish tone of accompanying communications and the Fed’s commitment to extend its ultra-accommodative policies, which further depressed Treasury yields and the dollar. The FOMC voted unanimously to maintain policy rates in a range of 0-0.25%, matching market expectations, but the dovish atmospherics weighed on Treasury yields across maturities, pulling 10-year Treasury yields to their lowest level since early March. Sliding interest rates, along with the Fed’s dim growth outlook, sent a broad dollar index to its lowest level in nearly two years yesterday, although it steadied overnight. The accompanying statement reiterated the Fed’s commitment to use its “full range of tools to support the US economy in this challenging time” and to achieve the objectives of its dual mandate, namely full employment and price stability at 2% inflation. Regarding the anticipated policy pivot this fall, the Fed’s communications provided only hints, with Chair Powell indicating that any enhanced guidance would be referenced to existing policy frameworks. On the timing, he noted that the FOMC was still conducting its monetary policy strategy review but would conclude in the “near future,” suggesting that the September meeting would be the venue for rollout. Chair Powell also stated that the Fed will sustain its historic easing until confident economy has “weathered recent events.” In the meantime, he “thinks the most central fact or the most central driver of the path of the economy is the virus,” and as such “in the broad scheme of things, there will be a need both for more support from [the Fed] and more fiscal policy.” In the near term, Chair Powell said the Fed does not see inflation on the horizon yet, calling the pandemic “a disinflationary shock” though he noted that “there’s a lot of discussion over how this might lead to inflation over time.”

Equities Fluctuate Ahead of Key Earnings Releases

Amid the busiest stretch of second quarter (Q2) earnings season, US stocks continue to alternate between gains and losses this week, with caution reemerging ahead of today’s consequential reports. With Q2 earnings season thus far sending mixed messages amid a high degree of upside surprises on headline numbers but lackluster details and guidance, today’s bevy of reports from high-flying tech giants and an array of other corporate bellwethers could provide greater directionality to the broader stock indexes. The spotlight is on Apple, Amazon, Google, and Facebook, all of which report after the closing bell. Shares of these four tech giants all rallied 1-2% yesterday despite already lofty valuations and the grilling their CEO’s received before the House Judiciary Committee on antitrust, data privacy and anticompetitive practices. Other companies issuing results today include UPS, DuPont, Eli Lilly, Comcast, Valero Energy, Proctor & Gamble, Mastercard, and Yum! Brands before the opening bell, with reports due from Ford, Shake Shack, US Steel, Expedia, MGM Resorts, Caterpillar, and Exxon Mobil alongside the tech giants after markets close. Yesterday, AMD was a standout performer, capitalizing on the travails of its competitor Intel, while Starbucks also impressed analysts despite a revenue plunge. Results from traditional economy bellwethers GM, GE, and Boeing, however, were less upbeat and shares of all three retreated following their releases. With 229 of S&P 500 companies having reported, 83.4% of results have featured a positive earnings-per-share (EPS) surprise and 65.5% have topped revenue estimates. However, aggregate growth of sales and earnings are down 9.6% and 14.2%, respectively, thus far year-on-year.

Additional Themes

US Economic Data in Focus – GDP for Q2 is expected to plummet 34.5% after a 5.0% Q1 contraction, although estimates range from -25% to -40%. Meanwhile, after last week’s tally of initial jobless claims increased for the first time since March, another increase is expected in today’s reading of new filings for the week ending July 25th, from 1.416 million to 1.445 million.

EU Growth Figures Meet Expectations – German GDP was slightly worse than expected, contracting 10.1% quarter-on-quarter versus a -9.0% forecast, following a 2.0% retrenchment in Q1. EU economic confidence gauges were relatively steady. The euro is dipping just below two-year highs versus the dollar.

Summary and Price Action Rundown

Global risk assets are modestly positive this morning amid the ongoing barrage of major corporate earnings reports, while investors await a Federal Reserve decision and monitor wrangling on Capitol Hill over the latest pandemic stimulus bill. S&P 500 futures indicate a 0.2% higher open after yesterday’s decline took the index back into slightly negative territory for the year, while choppiness continued in the tech-heavy Nasdaq. Equities in the EU and Asia were mixed overnight. The dollar is extending its downtrend, while longer-dated Treasury yields are edging up, with the 10-year yield at 0.59%. Brent crude prices are up toward $44 per barrel.

Federal Reserve Decision in Focus

Though no major changes are expected to current monetary settings, analysts will be highly attuned for any signals on impending policy shifts at the September meeting. In a bit of housekeeping yesterday, the Fed announced it would be extending its credit lending facilities through the end of the year. The myriad of facilities originally set to expire at the end of September will now run through to 2021. Later today, at the conclusion of the July meeting, the FOMC will release its key interest rate decision, with no change expected again. At the June meeting, the Fed left the target range for its federal funds rate unchanged at 0-0.25%, matching market expectations. However, the accompanying communications were more dovish than anticipated, and all but two of the FOMC participants expected it would appropriate to keep rates at zero through 2022. Meanwhile, the Fed reinforced its commitment to maintain “smooth market functioning” by promising to maintain its Treasury and mortgage purchases “at least at the current pace” of $80bn Treasuries and $40bn of mortgage backed securities (MBS) a month “over coming months,” as opposed to the open-ended period of the pandemic response in April minutes, easing from its peak of purchasing $300 billion in securities during the early days of pandemic-related shutdowns in the US. With interest rates and quantitative easing likely to remain steady, the focus will be on any additional information on a potential pivot to enhanced guidance or perhaps even some degree of specific yield-curve control at the September meeting. Additionally, the Fed Chair Powell will likely continue to advocate for augmented fiscal support to underpin the expansion.

Earnings Convey Mixed Messages

Amid the busiest stretch of second quarter (Q2) earnings season, caution took hold yesterday after a decidedly mixed set of results as analysts brace for key releases from IT giants and other household names later this week. Yesterday featured the earnings releases before the opening bell from 3M, DR Horton, Pfizer, Raytheon, JetBlue, and McDonalds, which reflected widely varied performance. On the downside, 3M, McDonald’s, and JetBlue missed on earnings consensus estimates, though the latter two beat depressed revenue projections. Industrial conglomerate 3M had the worst share price response, losing 4.8% after reporting a plunge in demand across its business lines and an organic revenue decline of 13%. McDonald’s saw store sales drop 24%, though noted its drive-thru and delivery performance offset major losses. Its shares fell 2.5%. DR Horton, Pfizer, and Raytheon all beat earnings and revenue projections for the second quarter, though only Pfizer stock managed to rise as the others were hit by profit-taking. After yesterday’s closing bell, Visa, Starbucks, Aflac, eBay, and AMD also reported mixed results, though AMD and Starbucks outperformed notably, sending their shares higher in pre-market trading. With 194 of S&P 500 companies having reported, 83.5% of results have featured a positive earnings-per-share (EPS) surprise and 65.8% have topped revenue estimates. However, aggregate growth of sales and earnings are down 8.7% and 14.9%, respectively, thus far year-on-year.

Additional Themes

Strategic Government Support Lifts Kodak – Amid increased urgency from the pandemic, the Trump administration’s policy push to re-shore strategic manufacturing from overseas took a step forward. Eastman Kodak stock jumped 207.6% yesterday after soaring over 300% at the outset of trading after it was announced that the company had received a $765 million government loan to expedite domestic production of drugs for several medical conditions. The loan is reportedly part of an effort to reduce US reliance on foreign sources of medication and drugs according to the International Development Finance Corporation (the successor to the Overseas Private Investment Corporation). The loan has been issued under the Defense Production Act. The loan has a 25-year term and is estimated to create around 350 jobs.

Pandemic Relief Bill Negotiations Grind Onward – With the battle lines drawn over key issues such as augmented unemployment benefits, aid for states and municipalities, and relief for renters, House Speaker Pelosi, Senate Minority Leader Schumer, Treasury Secretary Mnuchin, and White House Chief of Staff Meadows have been meeting. Though all are aiming for a package by the end of the week, concerns about timeline slippage are growing. Both the House and Senate appear poised to wait until agreement to try to pass anything further.

Looking Ahead – Do You Like Surprises?

This year has featured a jarring array of unexpected events, most of them decidedly unpleasant, and market participants are bracing for more to come. To borrow Donald Rumsfeld’s now-famous formulation, “unknown unknowns” are, by definition, impossible to predict, though nobody seems to be ruling anything out at this point given what 2020 has already thrown at us. Meanwhile, the “known unknowns” are certainly still capable of producing significant shocks.

Corporate reporting for the second quarter was almost certain to produce surprises both the upside and downside given the dearth of management guidance due to impenetrable Covid-19 uncertainties. Although earnings season is still in its early stages, surprises have indeed been the norm, as US megabanks blew estimates out of the water on the trading and investment bank side, but also exceeded the expected levels of credit provisioning, highlighting downside risks to the economic outlook. This wide dispersion around estimates is expected to continue with next week’s dense calendar of earnings announcements.

Questions still surround the two high-profile fiscal packages that are in the process of being negotiated in the US and EU, with both generally expected to be finalized by the rapidly approaching month-end. The wrangling is expected to be intense on both of these pandemic relief bills, but the expectation is for eventual compromise and agreement on a significant figure for each that is capable of providing real support to both economies. The predominant risk in the EU negotiation is for disappointment if the so-called Frugal Four countries (Netherlands, Denmark, Sweden, and Austria) refuse to compromise. In the US, there is upside and downside potential for the bill given the propensity for recent budget negotiations to expand the pie rather than make tough decisions, but there is certainly a meaningful risk of disappointment as well as the House Democrats, Senate Republicans, and Trump administration are finding less common ground than in the case of the CARES Act.

The Federal Reserve is working hard not to surprise the markets, with a veritable barrage of communications on a seemingly daily basis, but investor nonetheless remain wary of anticipated details of what seems to be an impending policy pivot. The constant din of fed speakers is not entirely unanimous but appears to be pointing broadly toward a shift in favor of enhanced forward guidance, predicated upon their traditional inflation target of 2%. It does seem unlikely, particularly ahead of an election when major monetary policy making tends to be inauspicious, that the Fed would make any sudden moves to startle investors, such as unexpectedly instituting yield curve control or taking interest rates into negative territory.

Last year featured a steady diet of nasty surprises on the US-China front, but ultimately with the Phase One trade deal being signed early this year, expectations for a tense equilibrium have settled in. Recent Trump administration actions to counter China on the tech and investment fronts, as well as retaliation for Beijing’s posture toward Hong Kong and repression in western China, have increased the degree of uncertainty among market participants regarding this key relationship. Speculation over a major White House policy escalation against China tend to be linked to the belief that President Trump may have to pull a spectacular October surprise in order to close the polling gap between himself and Joe Biden.

Polling data has been likened to intellectual junk food – quick and easy to digest, sometimes quite tasty, but ultimately unsatisfying and genuinely bad for you if you consume too much. Skepticism over the validity of political polls has increases significantly due to its notoriously spotty track record in recent years, with high-profile misfires over Brexit and the US election in 2016. On its face, President Trump’s current deficit to Joe Biden looks substantial enough to subsume any statistical oddities, but market participants are well aware that polls in swing states, which will decide the outcome, look meaningfully closer. They also note that Trump voters are thought to be quite shy with pollsters about their intentions, and that races traditionally tighten into the actual election day, which is still an eternity away in from a political standpoint. In short, this race is far from over.

Still, an October surprise by President Trump is seen as highly likely and the most common areas of speculation tend to be, as mentioned above, some kind of anti-China policy barrage, with some even floating the potential for outright geostrategic confrontation. More likely, we believe, is that Trump’s major moves in the fall designed to tip the political scales will be more targeted at Joe Biden in terms of alleged dirt or announced investigations. Unlike an offensive against China, this sort of approach has less likelihood of major market blowback.

Looking ahead to next week, the economic calendar is relatively light, with global PMIs for July featuring prominently, as Q2 earnings reporting season rolls on.

US Second Quarter Corporate Earnings:

Next week is dominated by ongoing US corporate earnings reporting, with the calendar featuring results from IBM, Halliburton, Coca-Cola, Lockheed Martin, Snap, Capital One, KeyCorp, Northern Trust, CSX, Tesla, Microsoft, Southwest Airlines, AT&T, Twitter, American Airlines, Honeywell, Verizon, Schlumberger, Royal Caribbean, and Intel.

Global Economic Calendar: Summer lull

Sunday

This upcoming weekend starts the weekend with the Loan Prime Rate Decision in China. The People’s Bank of China held its benchmark interest rates steady for the second straight month at its June fixing after the central bank maintained borrowing costs on medium-term loans last week, as policymakers adopted a wait-and-see approach amid tentative signs of economic recovery. The one-year loan prime rate was left unchanged at 3.85% from the previous monthly fixing while the five-year remained at 4.65%.

Monday

The focus on Monday will be Japanese Inflation Rate for June, which comes out after markets close that day. Japan’s consumer price inflation stood at a three-year low of 0.1% year-on-year (y/y) (flat, month-on-month (m/m)) in May, in line with market estimates, as the pandemic continued to hamper consumption. Prices fell further for transport & communication (-1.7% versus -1.2% in April), amid slumping oil prices. In contrast, inflation edged up for housing (0.8% vs 0.7%) while it remained unchanged for medical care (at 0.5%); clothing & footwear (at 1.4%) and food (at 2.1%). Core consumer prices, which exclude food and energy, dropped 0.2% y/y (the same pace as in April) and compared with market consensus of a 0.1% drop.

Tuesday

Tuesday morning, the focus will be on the Chicago Fed National Activity Index for June. The index rose to a record high of 2.61 in May from a downwardly revised record low of -17.89 in April as some lockdown restrictions caused by COVID-19 epidemic were lifted. All four sub-indexes made positive contributions in May with production and employment-related indicators leading the gains.

In the evening, Japanese manufacturing for this month will be the focus. The AU Jibun Bank Japan Manufacturing PMI was revised higher to 40.1 in June from a flash reading of 37.8, amid the prolonged impact of the COVID-19 pandemic on activity. The latest reading signaled a 14th consecutive month of contraction as new orders, output, employment and purchasing activity continued to fall at sharp rates. On the price front, selling prices dropped as businesses strived to stimulate sales, while input cost rose following a decline in May. On the other hand, sentiment jumped back into positive territory for the first time since February. Meanwhile, the Services PMI was revised higher to 45.0 compared to May’s 26.5. It was the highest reading since February as restrictions lifted.

Wednesday

The priority Wednesday will be the number of US Existing Home Sales last month. Sales of previously owned houses in the US dropped 9.7% m/m (26.6% y/y) from the previous month to a seasonally adjusted annual rate of 3.91 million units in May, below market expectations of 4.12 million. It is the lowest reading since 2010 and the steepest annual drop in nearly forty years. Declines were seen in all regions, although the Northeast experienced the greatest drop. The median existing-home price for all housing types in May was $284,600, up 2.3% from May 2019 ($278,200).

Thursday

Early Thursday morning we’ll get a look at consumer confidence in Germany. The GfK Consumer Sentiment indicator for Germany rose to -9.6 heading into July from an upwardly revised -18.6 in the previous month and compared with market consensus -12.0. Both economic and income expectations improved, as well as propensity to buy, following the gradual lifting of restrictions imposed to contain the coronavirus. The gauge for business cycle expectations jumped 18.9 points to 8.5, the highest reading since January 2019 and far above its long-term average of zero.

Just before markets open, Initial Jobless Claims will be released. The number of Americans filling for unemployment benefits stood at 1.30 million in the week ended July 11th, little-changed from a revised 1.31 million claims in the prior week and above market expectations of 1.25 million. This was the smallest week-on-week decline since claims started to fall after peaking in March. The latest number lifted the total reported since March 21st to 51.3 million.

Shortly after, we will get a look at Consumer Confidence in the Eurozone. The consumer confidence indicator in the Eurozone was confirmed at -14.7 in June, compared with May’s -18.8, on the back of households’ much improved expectations in respect of their financial situation, their intentions to make major purchases and, particularly, the general economic situation. Same as in May, households’ assessments of their past financial situation deteriorated, but on a much smaller scale.

Friday

Friday starts with several Markit PMI datapoints, beginning with the Eurozone. The IHS Markit Eurozone Composite PMI was revised higher to 48.5 in June from a preliminary estimate of 47.5 and compared to 31.9 in May. The reading pointed to the softer contraction in private sector activity in four months, as restrictions related to the coronavirus pandemic eased. Both manufacturing output (PMI at 47.4 vs 39.4 in May) and services activities (48.3 vs 30.5 in May) shrank at the weakest pace in four months. Though the Manufacturing PMI was revised higher to a four-month high, the latest survey suggested the Eurozone manufacturing sector remained in contraction territory for the past 17 months. Output and new orders declined at a softer pace as more businesses restarted operations following weeks of closure due to the coronavirus pandemic. Backlogs of work outstanding fell for a twenty-second successive month and employment dropped for a fourteenth month in a row. Purchasing activity also remained depressed. On the price front, both input costs and output charges continued to decline. Finally, confidence about production in the year ahead returned to positive territory and services optimism hit a four-month high during June.

Not long after the Eurozone, we will get Markit PMI for the United Kingdom. The IHS Markit/CIPS UK Composite PMI came in at 47.7 in June, little-changed from a preliminary estimate of 47.6 and compared to the previous month’s 30.0. Manufacturing production rebounded 9.4 points to 50.1 and service activity contracted at a softer pace, 47.1 compared to the previous month’s 29.0, in June as the economy reopened following months of disruption caused by the coronavirus pandemic. Manufacturing production rose slightly for the first time in four months, while new order intakes and employment fell at softer rates. On the price front, input costs rose the most in a year, although at mild pace, while output charges also increased. Looking ahead, business sentiment rose to a 21-month high in June due to clients reopening, an expected further loosening of COVID-19 restrictions and hopes that markets would revive at home and overseas to help recover growth lost during the pandemic.

Coming back to an American focus, lastly, we’ll get US Markit PMI. The IHS Markit US Composite PMI was revised higher to 47.9 in June from a preliminary estimate of 46.8 and compared to the previous month’s 37.0. Much softer rates of contraction were reported across the manufacturing and service sectors as the economy began to reopen following the coronavirus-related restrictions. New order inflows stabilized, and employment fell at softer pace, while excess capacity remained as backlogs of work continued to decline. On the price front, cost burdens were up for the first time since February, with private sector firms partly passing on higher costs to clients. Finally, companies expressed optimism towards the outlook for output over the coming year for the first time since March.

Next week, our interest concludes with New Home Sales in the United States. Sales of new single-family homes in the United States jumped 16.6% m/m (12.7% y/y) to an annualized rate of 676 thousand in May, beating forecasts of a 2.9% rise. However, data for April was revised sharply lower to 580 thousand from 623 thousand. Still, May’s figure is the highest in three months. There were 318,000 new homes on the market, down 2.2% from April. At May’s sales pace it would take 5.6 months to clear the supply of houses on the market. The median new house price rose $5,200 from a year ago to $317,900.

Summary and Price Action Rundown

US equities resumed their tech-led uptrend today ahead of key earnings releases later this week, the dollar’s ongoing downtrend accelerated, and investors continued to monitor signals from negotiations on Capitol Hill over the next pandemic relief bill. The S&P 500 retraced Friday’s downside to edge back into positive territory year-to-date but remained shy of last Wednesday’s peak for the pandemic. The tech-heavy Nasdaq erased last week’s rare underperformance. Equities in the EU and Asia were mixed. Longer-dated Treasury yields moved above March lows, with the 10-year yield at 0.62%, while more upbeat EU data lifted the euro and sent the dollar to a new multi-month low. Brent crude fluctuated above $43 per barrel.

Details Awaited on Senate Republican Stimulus Bill

Negotiations are set to heat up over the draft bill being crafted by Senate Leader McConnell. Republicans most notably have ramped up their rhetoric on cutting the soon-to-expire $600/week benefits down to a sliding scale of 70% of previous wages earned. The 70% payment scheme, according to several estimates, would take anywhere from two to five months to roll out as states will face significant difficulties in implementation compared to the flat rates previously used. Republican leaders have addressed the issue by suggesting a $200/week flat payment while states work on adjusting. This proposal is likely to be the main point of contention between the parties as Speaker Pelosi has made clear her intention of defending the $600 payments through the end of the year. Other provisions include liability protections for hospitals, schools, and nonprofits, $105 billion allocated towards school reopening, $16 billion for enhanced testing measures, a second round of the Payroll Protection Program (PPP) targeted at SMEs that have seen 50% or greater falls in revenue, according to Treasury Secretary Mnuchin, and the proposal to issue another set of $1200 direct payments to individuals and families. Friday’s CNN interview with Larry Kudlow also confirmed a plan to lengthen the period of the federal eviction moratorium that is set to expire.

Senate Minority Leader Schumer lambasted the previously-reported provisions as inadequate, failing to effectively cover issues ranging from rental assistance to state and local government funding, points that are staunchly defended in the Democrat’s previous HEROES Act proposal that passed in May. Where the GOP plan reports only loosening guidelines on spending previous CARES Act funding for states and localities, with no new added stimulus, the Democrats originally proposed nearly $1 trillion in spending to plug budget gaps from emergency relief spending and lost tax revenues.

Given the likelihood that negotiations will drag further into August than hoped, White House officials have already begun pushing a “skinny” version of stimulus, with both Chief of Staff Meadows and Secretary Mnuchin on Sunday news shows advocating a narrow focus on unemployment benefits while kicking future decisions down the road to a possible September stimulus. A narrow package has been labeled unacceptable by Democrats who claim the provisions are necessarily linked to each other, claiming that passing certain provisions will extend benefits to some while leaving others to fall through the cracks unaddressed. – MPP view: With the July 31st deadline for enhanced unemployment benefits approaching, debates over the coming week will likely push Republicans towards the bargaining table as a “no deal” scenario is politically unacceptable and it is widely understood that the bill will increase from the first draft $1 trillion anyway.

Stocks Rise Ahead of Earnings Barrage

Going into the busiest stretch of second quarter (Q2) earnings season and key releases from IT giants, stocks marched higher with tech again taking the lead. With last week marking the first third of S&P 500 companies to report Q2 earnings, analysts are still groping for consistent themes heading into this week’s major lineup of reporters. With 129 of S&P 500 companies having reported, 84.9% of results have featured a positive earnings-per-share (EPS) surprise and 67.4% have topped revenue estimates. Both percentages place higher than their respective five-year averages. Tomorrow, Visa, Pfizer, McDonald’s, 3M, Starbucks, AMD, Chubb, eBay, Aflac, and DR Horton report. Analysts will be focused on Visa’s payments volume since in May, as total US payments volume slumped 5% y/y. With shelter-in-place restrictions beginning to relax later in Q2, it is likely this will be reflected on payments volume, offsetting lagging cross-border revenues. AMD will fight to keep its recent price action hot-streak alive from Friday after Intel’s disappointing report last week disclosed that the company is looking to outsource its chip production to competitors like AMD. Chubb traded 1.9% lower amid expectations that, given the pandemic, the company has less growth in travel insurance, accident & health discretionary purchases, automobile insurance, and commercial lines of business. Lastly, DR Horton saw a significant 4.4% rise in share price today as analysts are expecting an earnings beat after estimates were recently revised upwards, which is usually an accurate indication of favorable trends for the company.

Additional Themes

US June Data Remains Strong – New orders for key US-made capital goods increased by the most in nearly two years in June and shipments accelerated driven by pent-up demand following the reopening of businesses. New orders for US manufactured durable goods rose 7.3% from the previous month in June, following a downwardly revised 15.1% jump in May and beating market forecasts of 7%. Demand for transportation equipment jumped 20%, mainly due to motor vehicles and parts (85.7%) while defense aircrafts and parts plunged 30.6%. Excluding transportation, new orders increased 3.3% and excluding defense, new orders increased 9.2%. Orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, jumped 3.3% after a 1.6% gain in May. Core capital goods orders were hit much less hard by Covid-19 than by the crash of 2008 and the subsequent credit crunch. Moreover, the bulk of the hit to second-quarter gross domestic product was in consumption—not capital spending. – MPP view: Backward-looking June data is being discounted, and rightly so. The dollar took a beating today, as more upbeat EU data (see below) sent the euro to a new 2020 high and its strongest level in two years.

German Business Gauge Points to Continued Rebound – The Ifo Business Climate indicator for Germany rose by 4.2 points from the previous month to a five-month high of 90.5 in July, recovering further from an all-time low reached in April and beating market expectations 89.3. The services component index rose from -6.0 to 2.0, positive for the first time since February. The gauge indicating firms’ projections for the next six months came in at 97.0 for July, up from the previous month’s 91.4 reading and better than market expectations of 93.7 following the easing of the coronavirus-induced lockdown. In the entire month of July, the country of 83 million has had less than 10,000 new coronavirus infections.

Summary and Price Action Rundown

Global risk assets have turned lower this morning amid a slew of major corporate earnings reports, while investors monitor wrangling on Capitol Hill over the latest pandemic stimulus bill. S&P 500 futures point to a 0.3% lower open after yesterday’s rally took the index back into positive territory for the year but fell short of last Wednesday’s peak for the pandemic. The tech-heavy Nasdaq erased last week’s rare underperformance with a 1.7% rally yesterday but is wavering this morning. Equities in the EU and Asia were mixed overnight. The dollar continues to sink lower versus its peers, while longer-dated Treasury yields are steady, with the 10-year yield at 0.61%. Brent crude prices are holding above $43 per barrel.

This Week’s Corporate Earnings Barrage Begins

US equities have been broadly supported but struggling to make upside headway during the first two weeks of second quarter (Q2) earnings reporting, as analysts await this week’s set of results featuring major tech giants and other US corporate bellwethers. With last week marking the first third of S&P 500 companies to report Q2 earnings, analysts are still groping for consistent themes heading into this week’s major lineup of results. With 155 of S&P 500 companies having reported, 84.8% of results have featured a positive earnings-per-share (EPS) surprise and 67.8% have topped revenue estimates. Both percentages place higher than their respective five-year averages. However, aggregate growth of sales and earnings are down 7.8% and 15.1%, respectively, thus far year-on-year. Today, Visa, Pfizer, McDonald’s, 3M, Starbucks, AMD, Chubb, eBay, Aflac, and DR Horton report. Pre-market releases have been mixed, with 3M undershooting earnings estimates and McDonald’s posting a steeper-than-expected decline in sales, while Pfizer and Raytheon both topped consensus forecasts. Among the later reports, Visa’s payments volume will be in focus, and DR Horton will provide insights on the US housing market, which has displayed great resiliency thus far during the pandemic. The rest of this week’s calendar features reports from major industry bellwethers, including GE, Boeing, GM, Qualcomm, PayPal, Facebook, UPS, Yum! Brands, Comcast, Proctor & Gamble, Mastercard, Ford, Apple, Shake Shack, Google, US Steel, Amazon, Expedia, Caterpillar, and Exxon Mobil.

Negotiations Begin in Earnest Over the Senate Republican’s Stimulus Bill Draft

Yesterday’s late afternoon release of the draft bill was the starting gun for what analysts expect will be a fraught negotiation, with trillions of dollars separating the two parties. The area of greatest urgency is enhanced unemployment benefits, with millions of American still out of work due to the pandemic and the current $600 per week boost expiring at month-end. The Republican proposal begins by cutting this to an extra $200 per week, then transitioning to a sliding scale based on 70% of previous wages earned but with a cap of $500 per week for the federal enhancement. Analysts suggest that this more complex scheme could take anywhere from two to five months to roll out as states will face significant difficulties in implementation compared to the flat amount previously used. Speaker Pelosi has made clear her intention of defending the $600 payments through the end of the year. Other provisions include liability protections for hospitals, schools, and nonprofits, $105 billion allocated towards school reopening, $16 billion for enhanced testing measures, a $60 billion top-up of the Payroll Protection Program (PPP) targeted at SMEs that have seen 50% or greater falls in revenue, and another set of $1200 direct payments to individuals earning less than $75K per year, plus some modest tax breaks related to business operations during the pandemic. Congressional Democrats have lambasted the provisions as inadequate, failing to effectively cover issues including rental assistance and state and local government funding support, both of which featured prominently in the Democrat’s $3.5 trillion HEROES Act proposal that passed in May.

Additional Themes

Two-Day Fed Meeting Kicks off Today – No major policy maneuvers are expected, though analysts will parse the accompanying communications for clues as to a potential policy pivot at the September meeting to some form of enhanced forward rate guidance. At the June meeting, the FOMC retained its current policy settings, as expected, and Chair Powell discussed the potential for yield caps and augmented guidance down the road, as the focus remained firmly on downside risks to the recovery.

Gold Prices Tag All-Time High – With the dollar in a downtrend, global interest rates at historic lows, deficits soaring, and geostrategic tensions simmering, factors have been aligned for gold price upside. The yellow metal registered an all-time high overnight near $2000 per ounce after an 8.3% month-to-date gain, and analysts are generally calling for more upside give the persistence of the upside drivers. Silver prices have also skyrocketed, soaring nearly 30% in July. –

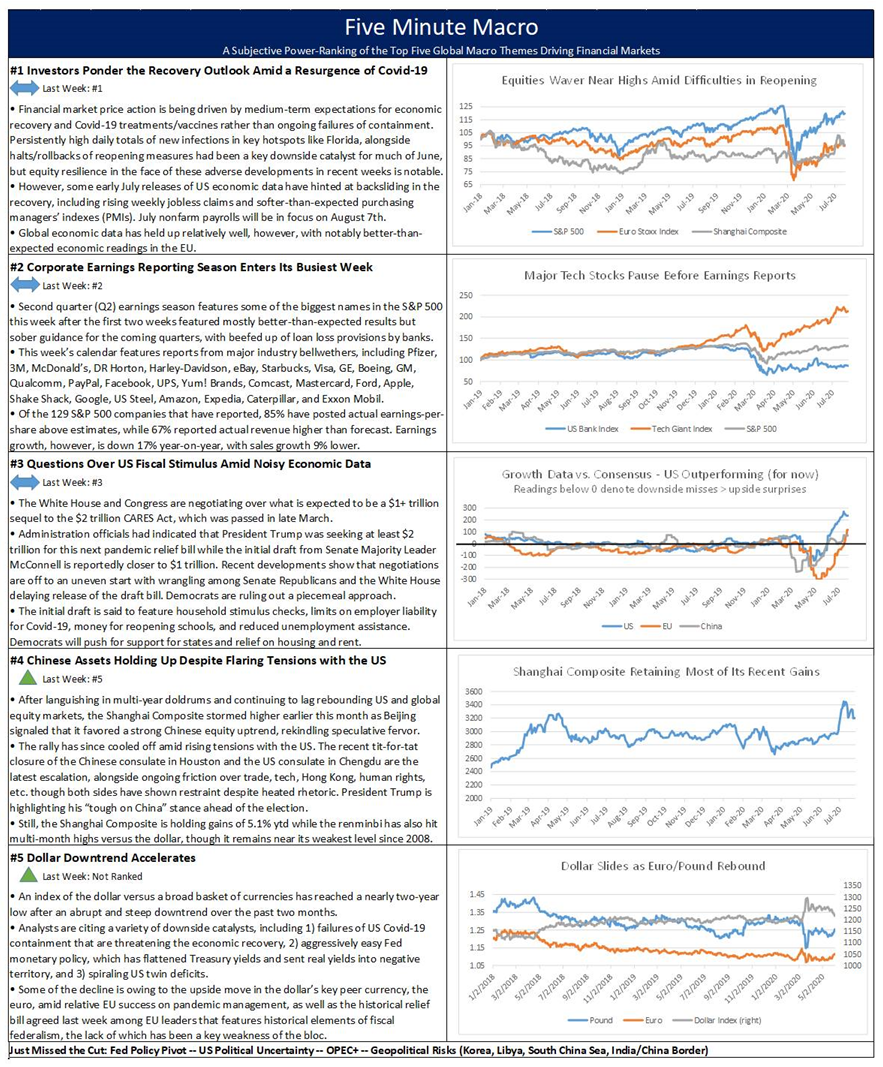

Covid-19 infection rates, corporate earnings and the state of CARES 4 remain the top three things driving markets this week. The Chinese asset rally moves up to fourth, while the quickly weakening Dollar enters in the final spot.

Summary and Price Action Rundown

Global risk assets are mostly higher this morning ahead of a week of major corporate earnings, key economic releases, and a Federal Reserve meeting. S&P 500 futures indicate a 0.4% higher open, which would retrace last week’s choppy 0.3% decline that took the index back into negative territory year-to-date after it registered a new high for the pandemic on Wednesday. The Nasdaq posted rare underperformance last week, falling 1.3% as high-flying IT shares reversed from lofty levels, but is set to rebound today ahead of major tech earnings this week. Equities in the EU and Asia were mixed overnight. The dollar continues to sink lower versus its peers, while longer-dated Treasury yields are declining, with the 10-year yield at 0.58%. Brent crude prices are holding above $43 per barrel.

Pivotal Week for Corporate Earnings

The second week of second quarter (Q2) earnings reporting again provided scant direction for stocks as analysts brace for this week’s busy calendar of results, featuring major tech giants and other US corporate bellwethers. Friday marked the close of the second week of Q2 earnings season with 181 of the S&P 500 companies reporting results to date. Thus far, 85.5% of results have featured a positive earnings-per-share (EPS) surprise and 67.7% have beaten revenue estimates, with both percentages being higher than their respective five-year averages. While this usually indicates positive trends, earnings and revenue estimates prior to the start of the quarter had been significantly lowered, with Q2 estimated earnings languishing in the doldrums at -44.7% year-on-year (y/y) two weeks ago. The current blended earnings decline, which combines actual results from companies that have reported and estimates of those that have not yet done so, has improved slightly to -42.4% from last week’s -44.1%. The blended revenue decline for the second quarter sits at -10.1%, rising from the revenue decline of -10.4% last week, and forming a trend of improvement from -10.8% two weeks ago. This week’s calendar features reports from major industry bellwethers, including Pfizer, 3M, McDonald’s, DR Horton, Harley-Davidson, eBay, Starbucks, Visa, GE, Boeing, GM, Qualcomm, PayPal, Facebook, UPS, Yum! Brands, Comcast, Proctor & Gamble, Mastercard, Ford, Apple, Shake Shack, Google, US Steel, Amazon, Expedia, Caterpillar, and Exxon Mobil.

US-China Tensions Remain Elevated but Restraint is Evident

China has closed the US consulate in Chengdu in retaliation for the US closure of the Chinese consulate in Houston, but Chinese assets were steady overnight and the lack of further escalation has eased concerns of a potentially major rupture in relations. Analysts had expected China to respond in kind after the US ordered China’s Houston consulate to be shuttered, though initial speculation had been that Beijing would shutter the US consulate in Wuhan. The US diplomatic presence in Chengdu is considered the more strategic of the two, as it is where the State Department monitors Tibet and the Western China region in general, which is a hotbed of human rights issues. However, no further measures were announced and Chinese assets steadied overnight. After sinking 3.9% on Friday amid the rising tensions, the Shanghai Composite eked out a 0.3% gain overnight, while the Hong Kong Hang Seng lost a modest 0.4% after closing 2.2% lower the prior session. The renminbi also advanced versus the dollar and is near its strongest level since March.

Additional Themes

GOP Draft of US Pandemic Relief Bill Expected Today – Though portions of the Republican’s draft $1 trillion stimulus plan have trickled out, the full text of the version crafted by Senate Majority Leader McConnell’s office is set to be released later today. Among the available details, the most notable is the new unemployment insurance scheme to replace the current $600/week benefits that are set to expire in a few days. The GOP unemployment insurance plan will focus instead on a 70% wage replacement benchmark. Additionally, the plan is said to include direct payments of $1,200 and $2,400 to individuals and families, $105 billion for reopening schools, targeted additional funds for the Payroll Protection Plan (PPP), $16 billion in additional funding for coronavirus testing, tax breaks for businesses to retain workers and retool for new safety protocols, and provisions for flexibility on state use of previous funding. The Trump administration has also backed off its demands for payroll tax cuts. Democrats will contest the absence of additional funding for state and local governments, as well as the lack of support measures for housing and rent. House Speaker Pelosi dismissed talk of a piecemeal approach to passing the bill but administration officials continue to advocate such an approach.

Dollar Downtrend Continues – An index of the dollar versus a broad basket of currencies has reached a nearly two-year low after an abrupt and steep downtrend over the past two months. Analysts are citing a variety of downside catalysts, including failures of US Covid-19 containment and aggressively easy Fed monetary policy.