Summary and Price Action Rundown

Global risk assets are pausing their ongoing rally this morning amid heightened US-China tensions while investors await more dismal US economic data and Federal Reserve communications. S&P 500 futures point to a 0.5% lower open, which would pare this week’s solid 3.8%, spurred by rising optimism over economic reopening and redoubled pledges of additional extraordinary monetary support from Fed Chair Powell. Year-to-date downside for the index has narrowed to only 8.0% and the decline from February’s record high is at 12.2%. Equities in the EU and Asia also posted moderate losses overnight. Longer-dated Treasury yields are steady, with the 10-year yield at 0.67%, while the dollar is flat in the middle of its recent trading range. Crude oil is extending its sharp uptrend from its lows, with Brent topping $36.

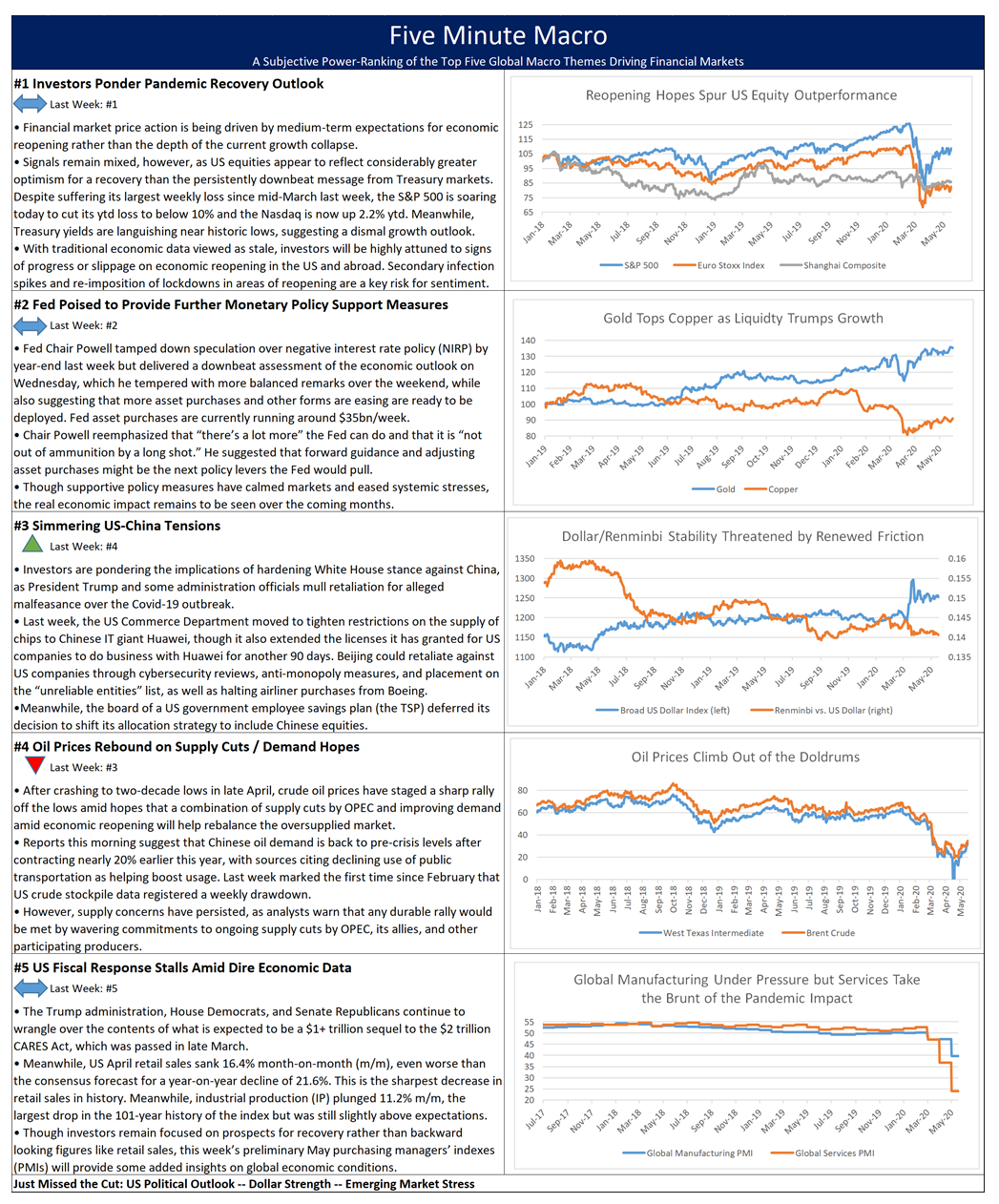

Investors Ponder the Ramifications of US-China Tensions

The US and China continue to trade barbs over a broad array of issues, with the Senate passing a bill targeting Chinese stocks that trade on US exchanges and President Trump turning up the rhetorical heat. Yesterday, the US Senate passed a bill with broad bipartisan support which could result in the eventual delisting of Chinese companies currently trading on US stock exchanges barring fulfillment of certain conditions. Specifically, the bill calls for listed companies to pledge that they are not controlled by a foreign power or government, and notwithstanding the generalized language, the sponsors of the bill made clear that it is specifically directed at Chinese companies. Also, if a company does not submit an audit for inspection by the Public Company Accounting Oversight Board for three straight years, its shares will be delisted from US exchanges. Though the House of Representatives is not yet taking up this legislation, analysts suspect that it will over the coming weeks and believe it will pass and be signed by President Trump. Shares of US-listed Chinese tech giants sold off on the headlines but mostly recouped their intraday losses, likely due to the relatively lengthy timeline for any enforcement actions (three years at least). A basket of Chinese ADRs fell as much as 3.9% from the intraday highs but closed only 0.6% lower on the day. Relatedly, shares of Luckin Coffee extended their precipitous plunge after reopening yesterday for trading on the Nasdaq following a suspension due to the revelation in April that management fabricated an enormous amount reported sales. The Nasdaq is set to delist Luckin Coffee pending a hearing and has indicated that it will tighten the accounting requirements for its listed companies. Separately, President Trump took to Twitter last evening to suggest that Chinese President Xi has a hand in the disinformation campaigns over the pandemic and that China is “desperate” for Biden to beat him in November’s presidential election. Early yesterday, tension had already been rising between China and the US, as Chinese officials reacted sharply to Secretary of State Pompeo’s recent statements on Taiwan, which Beijing are calling a violation of the “one-China” principle.

Fed Minutes Convey Caution as Investors Await Weekly Jobless Data

The minutes of the April 28-29 FOMC meeting released yesterday demonstrated continuity of the Fed’s historically accommodative posture in face of the Covid-19 pandemic as economic data remains severely depressed. Citing the extraordinary amount of uncertainty and considerable risk to the economy in the medium term, members noted that interest rates will be kept near zero until a recovery is firmly in place and reiterated their commitment to use their full range of tools to support the US economy. The outlook was generally dour, focusing on the risk that a second wave of the pandemic could lead to another round of lockdowns and drag the US economy deeper in recession, prompting a further jump in unemployment and renewed downward pressure on inflation. Fed Chair Powell will make more remarks today, as will Vice Chair Clarida and New York Fed President Williams. Meanwhile, today’s tally of jobless claims for the week ending May 16th are estimated at 2.4 million, which remains dismally high but would continue the declining trend over recent weeks and mark the lowest level since the pandemic began. For context, 3.0 million Americans filled for unemployment benefits for the week ending May 9th, down from 3.2 million the prior week, lifting the total reported to 36.5 million, equivalent to nearly a quarter of the working age population.

Additional Themes

Treasury Issues 20-Year Bond – Yesterday, traders noted a strong Treasury auction for its new 20-year bonds, which is the first time the maturity has been sold since 1986. Both the 10-year and 30-year bonds rallied following the sale of their new benchmark neighbor. In his testimony yesterday, Treasury Secretary Mnuchin indicated that he had turned down proposals of 50- & 100-year Treasury issuances because “demand is just not there.”

Turkey Cuts Rates – The lira has recovered modest losses today against the dollar after the central bank cut its policy rate for the ninth straight time from 8.75% to 8.25%. The lira has rallied in recent weeks after registering a record low against the dollar early this month.