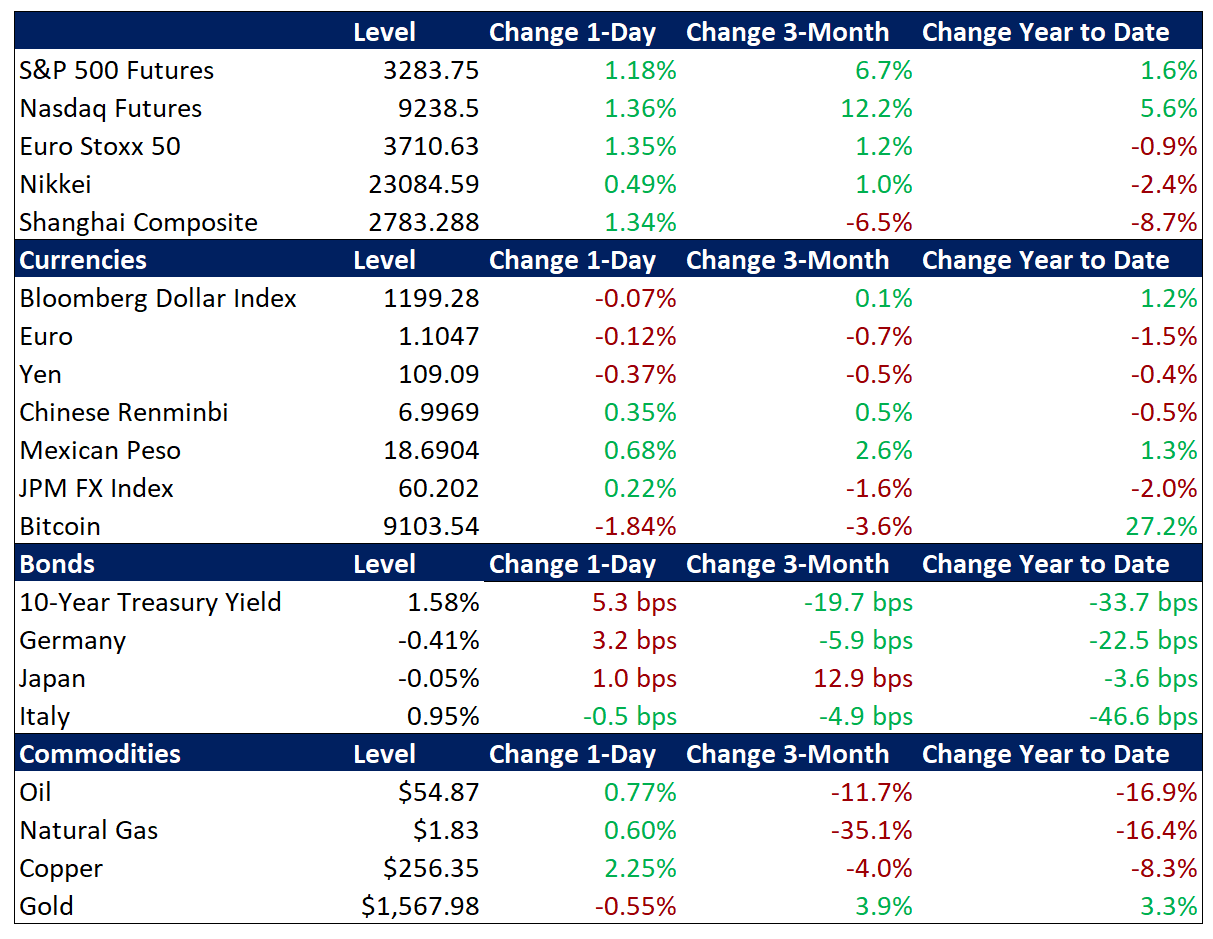

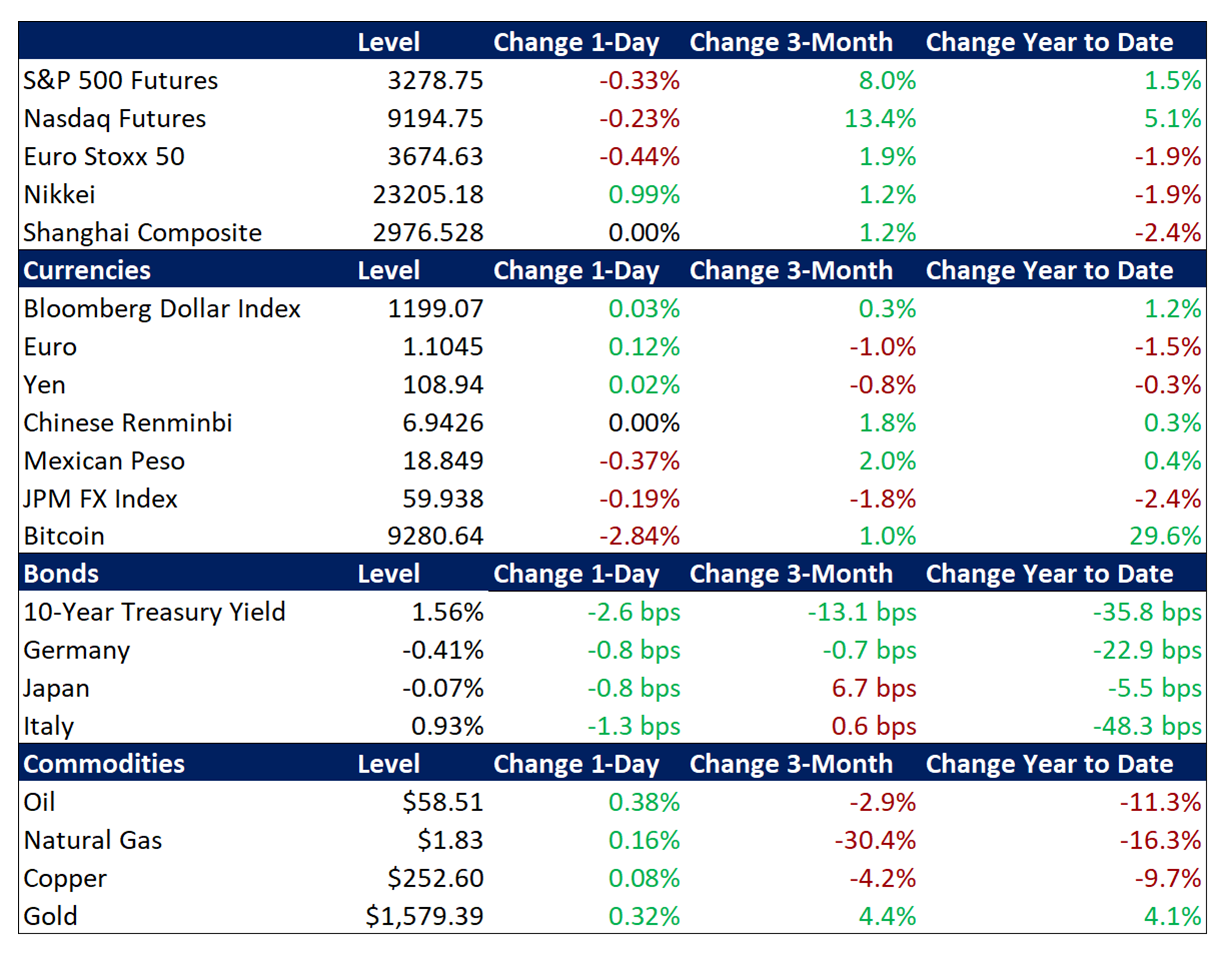

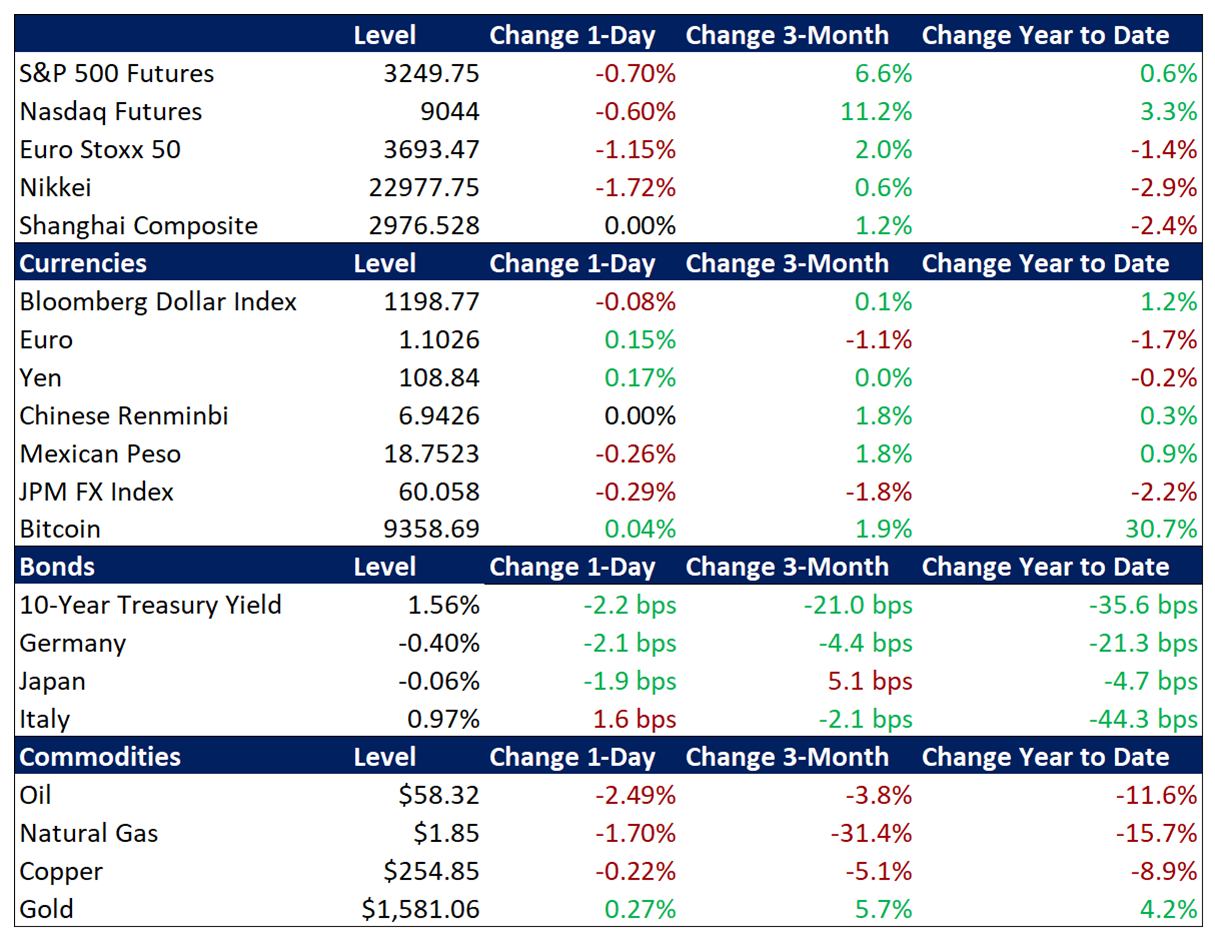

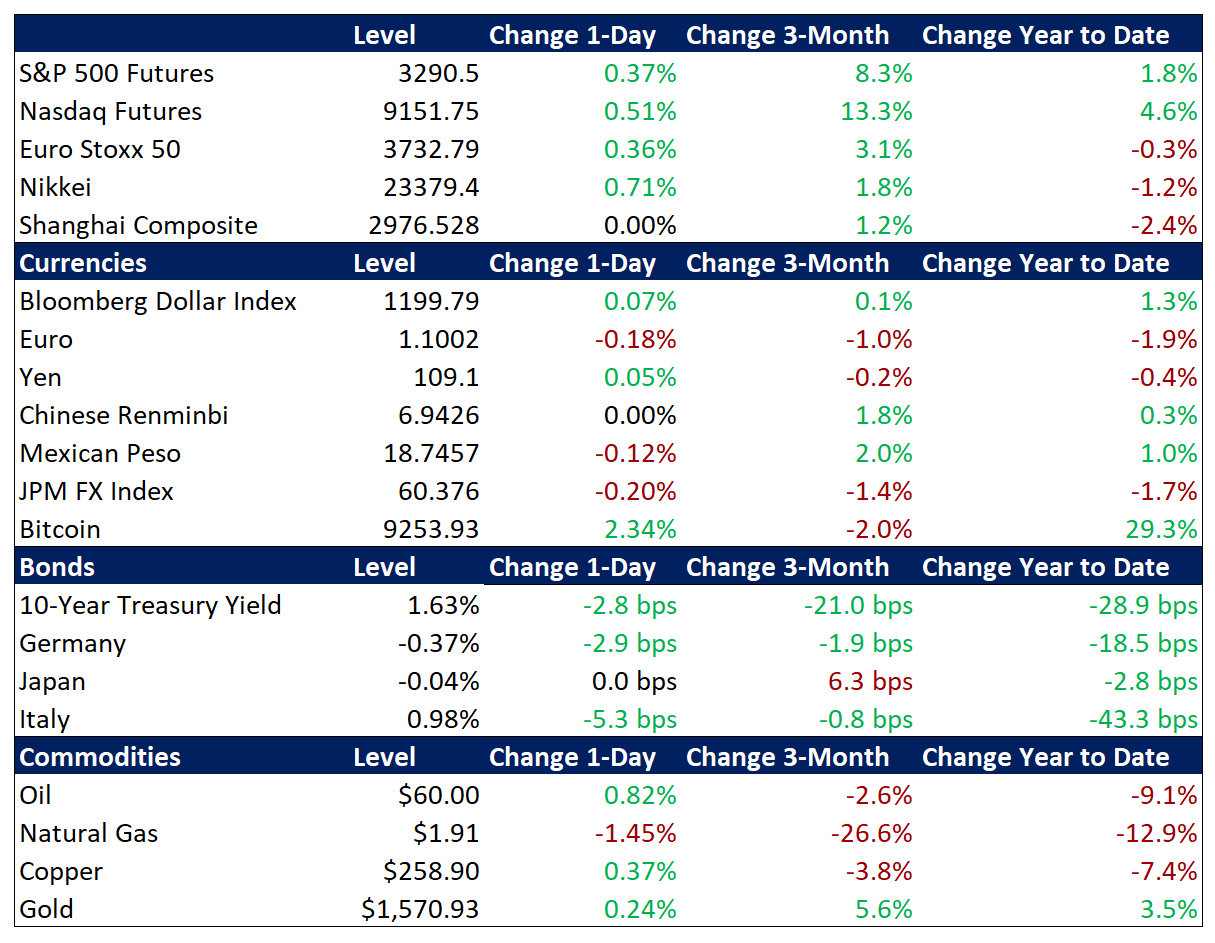

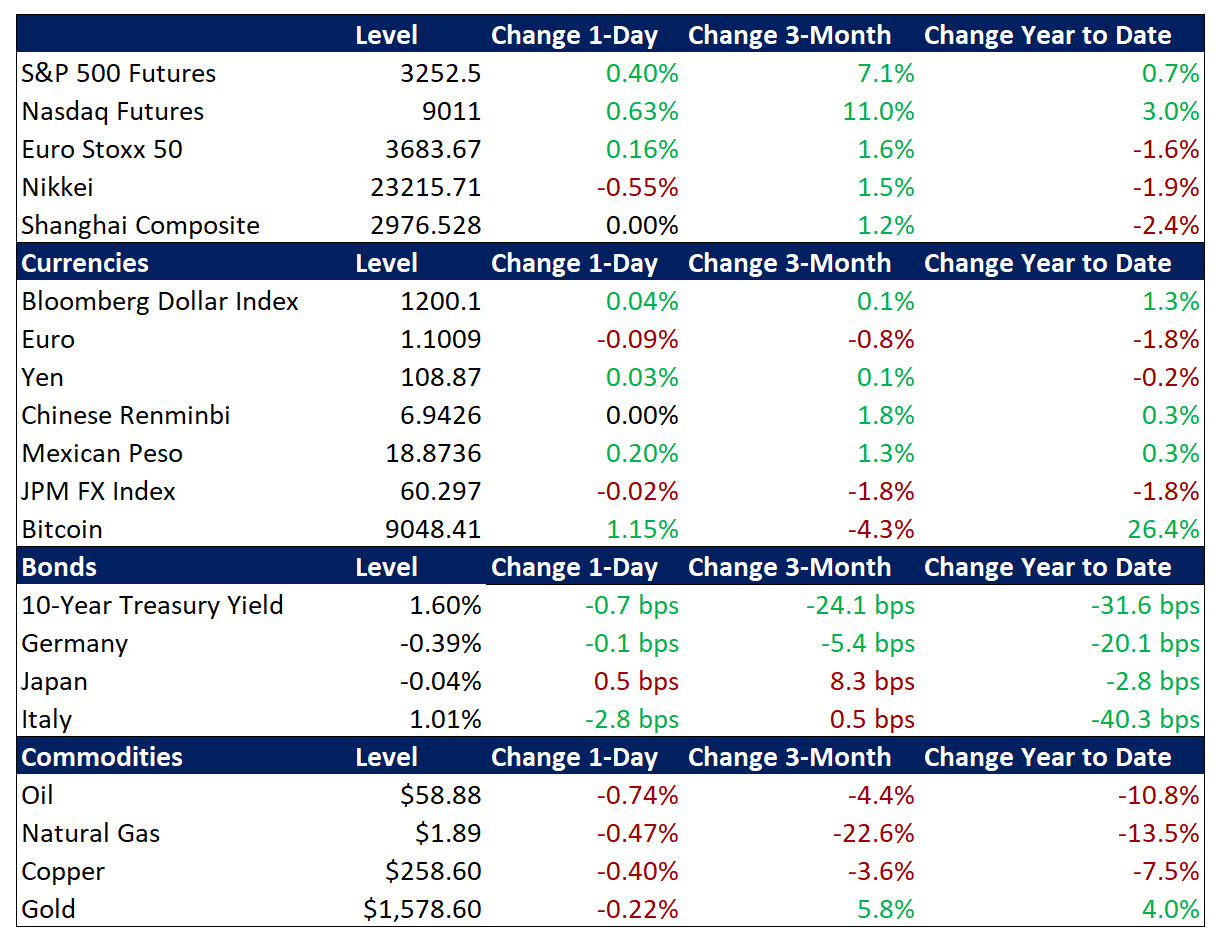

Summary and Price Action Rundown

Global risk assets are continuing this week’s sharp rebound as investors shake off outbreak fears amid reports of progress toward a treatment and data suggesting a slower spread. S&P 500 futures indicate a 0.8% gain at the open, which would bring the index nearly level with its record high from mid-January. Investors have seized upon a few encouraging developments this week in the ongoing efforts to combat the coronavirus, allowing the focus to shift back to supportive earnings and other positive factors, but the general mood remains cautious with volatility levels elevated. Overnight, equities in Asia followed the Shanghai Composite higher for a second straight session, while EU equities overcame early losses as analysts focused on reports of progress toward a vaccine for the coronavirus. As risk appetite continues to improve, Treasury yields are edging further above their recent three-month trough, but remain at very low levels, with the 10-year yield at 1.63% after starting the year at 1.92%. The dollar is flat and currency market volatility has remained generally subdued. Crude oil prices are rebounding this morning as an OPEC technical committee conference stretches to a second day, with the potential for a full cartel meeting as early as next week to consider emergency cuts.

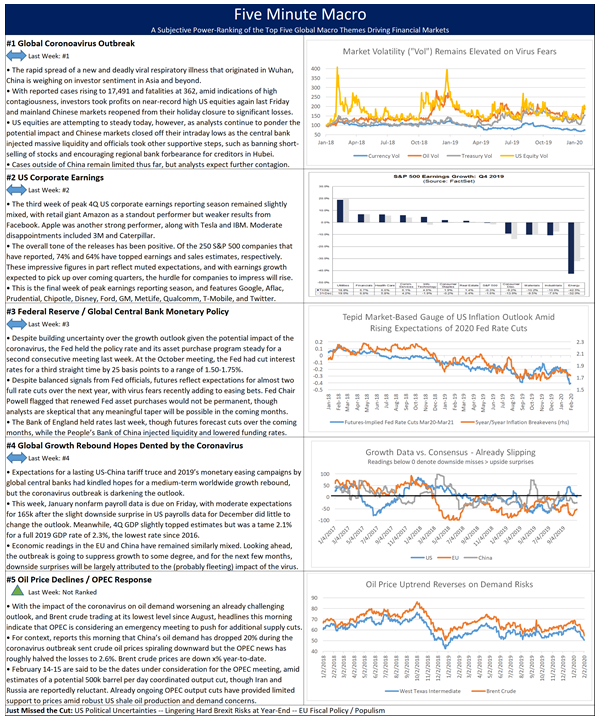

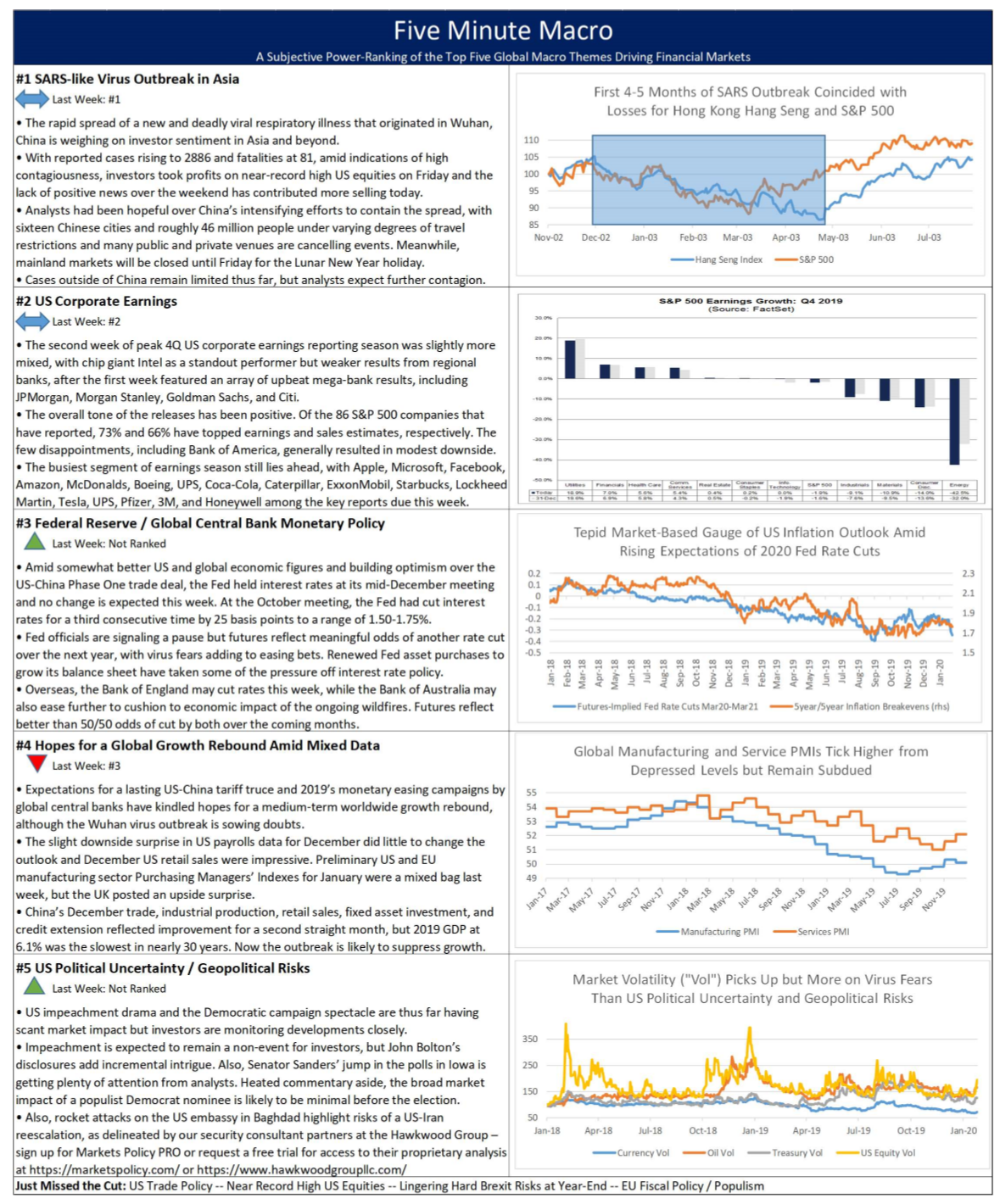

Hopes for Coronavirus Containment Fuel the Risk Asset Rebound

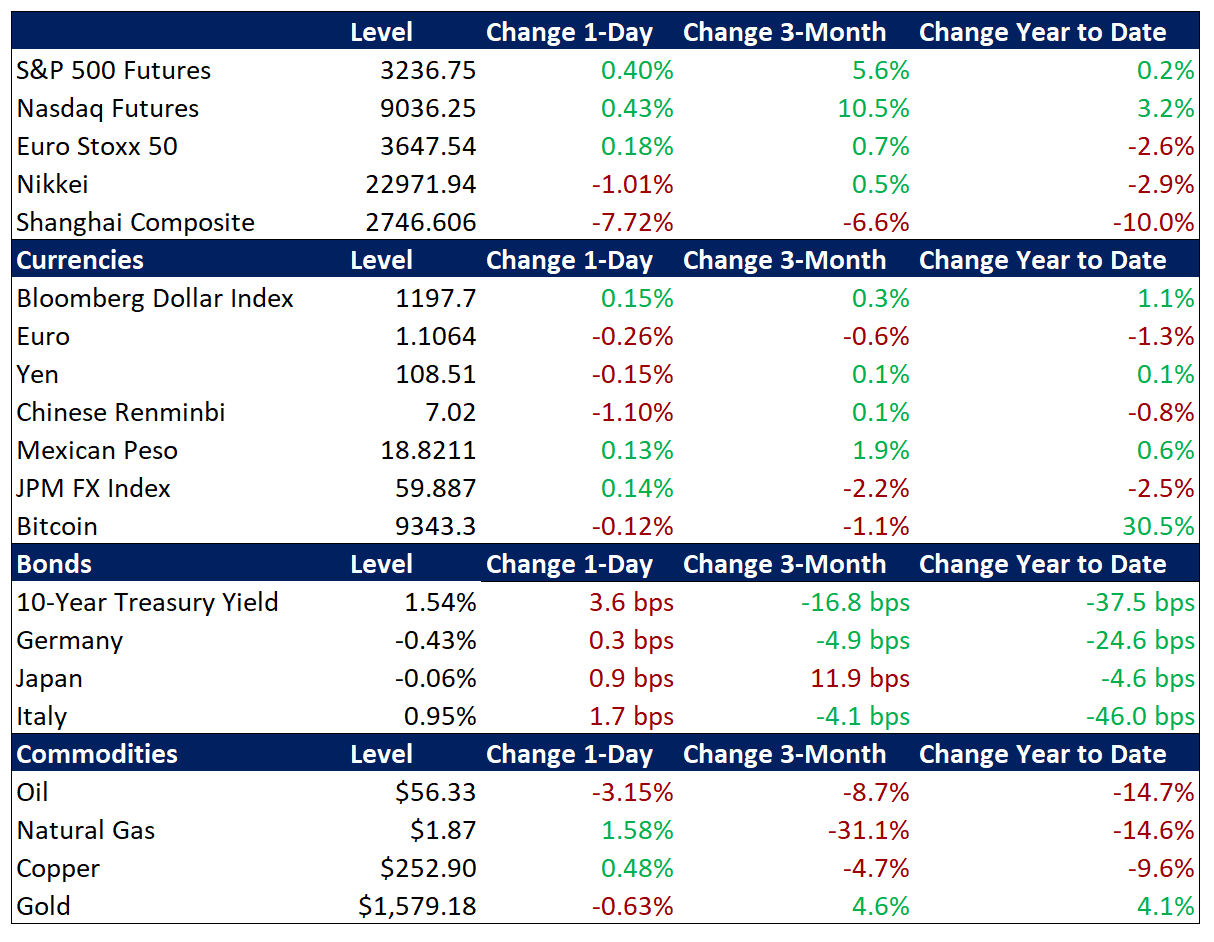

Investor sentiment is improving for a third straight session this week, levitating risk asset prices worldwide, amid hopes that the worst may be over for the outbreak. Reports overnight that UK scientists have made progress toward a vaccine, which some reports are calling a “breakthrough,” provided a further boost to already surging investor optimism over ongoing efforts to counter the coronavirus. Encouraging news over the past few days about the effectiveness of a drug produced by Gilead Sciences was underscored by efforts to secure a local patent for the drug in China. Headlines are also touting a possible slowdown in the infection rate, with 3,971 new reported cases yesterday versus 5,072 on Monday. Total reported infections have risen to 24,604 and fatalities to 494. The Shanghai Composite rallied for a second straight day, adding 1.3% to further retrace Monday’s sharp 7.7% loss. Official and unofficial state support is being credited with helping the index bounce back. The renminbi also continued to gain, appreciating 0.3% further past the closely-watched 7 to the dollar level.

Corporate Earnings Retain a Positive Tone Despite Some Uneven Results

Despite a few high-profile disappointments, fourth quarter (4Q19) corporate reports mostly continue to impress, while shares of Tesla extended their dizzying uptrend. Shares of Google fell 2.6% yesterday after the IT giant reported lower-than-expected revenue, with some key business components underperforming. Ford’s report after yesterday’s closing bell also missed estimates, sending its stock price 8.2% lower in pre-market trading. Disney’s results beat forecasts, but are still down 0.5% ahead of the opening bell. Of the 264 S&P 500 companies that have reported 4Q19 results, 75% have topped earnings expectations and 65% have beaten sales estimates. Today features GM, MetLife, and Qualcomm and the remainder of this final week of peak earnings reporting season brings results from Kellogg, Philip Morris, T-Mobile, Tyson Foods, and Twitter. Meanwhile, Tesla’s stock price surged another 13.7% yesterday after rallying 19.9% on Monday, putting the market capitalization of the electric car maker above $900 billion, with gains of over 110% so far this year. Tesla is one of the most heavily shorted stocks in the S&P 500, meaning that many speculators had bet that Tesla shares were overvalued and should trade lower, only to be forced to cover positions by buying back the carmaker’s stock at ever higher prices over the past month.

Additional Themes

Encouraging Pre-Virus Global Growth Data – The UK service sector purchasing managers’ index (PMI) for January registered a solid 53.9, rising from a preliminary estimate of 52.9. This put the final composite of both manufacturing and service PMIs for last month at 53.3, well above the earlier projection of 52.4 and at the gauge’s highest level since late 2018. For context, PMI readings above 50 denote expansion in the sector. In the EU, the service sector PMI for January matched its preliminary estimate at 52.5, rendering a composite January PMI reading of 51.3, extending the gradual improvement from last September’s multi-year low of 50.1. EU December retail sales data, however, undershot estimates, slowing to 1.3% year-on-year from 2.3% the prior month. Later today, analysts will note two separate readings of US service sector PMI, as well as a private sector jobs number, which is a prelude to Friday’s January nonfarm payroll data. These will be among the final economic data points before the impact of the coronavirus begins to distort global growth figures over the coming months.

Global Central Banks – The trend of ever easier monetary policy around the world continues apace today, with the Bank of Thailand unexpectedly reducing its policy rate by 25 basis points to a record low 1.0%, while Brazil’s central bank is set to cut rates at its meeting later today.